Earn with Nexo

Earn with Nexo

Bloomberg reports fastest rise in gamma as extreme speculation grips US stocks

A handful of US names are driving unprecedented moves in gamma, correlation, and dispersion, creating a feedback loop that could amplify volatility in either direction.

Stock market gamma just did something it has never done before. The measure of how sensitive options prices are to moves in their underlying assets surged to positive extremes at a pace that, according to Bloomberg, has no historical precedent.

The culprit is familiar: extreme speculation concentrated in a small cluster of US equities.

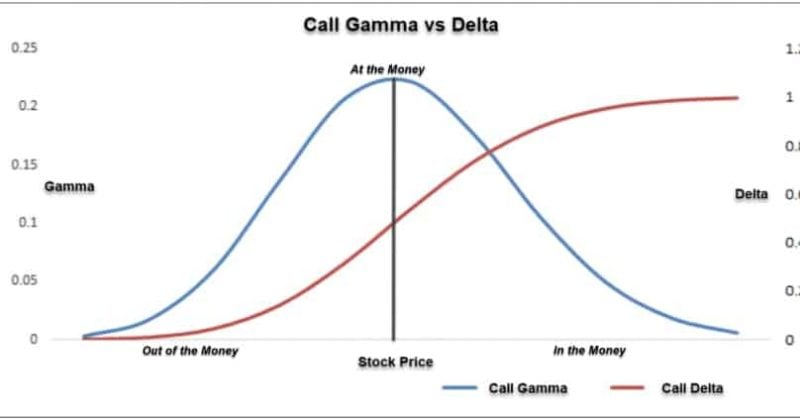

What gamma actually means (and why the speed matters)

Think of gamma as the accelerator pedal on a car that options dealers are forced to drive. When gamma is positive and rising, dealers have to buy stocks as prices go up and sell as prices go down. They become momentum amplifiers, whether they want to be or not.

Simon White, Bloomberg’s macro strategist, put it plainly. “Stock market gamma has jumped higher in one of the most rapid moves seen,” he noted, framing it as a direct consequence of speculative activity clustered in a handful of names.

What makes this moment unusual is not just the level of gamma but the speed of the transition. Markets went from deeply negative gamma, where dealer hedging amplifies selloffs, to near-record positive territory in a compressed timeframe.

The numbers behind the speculation

The breadth of the recent rally tells part of the story. Of 3,807 option-listed stocks tracked during a recent Monday session, 3,262 closed higher. That is 86% of the entire universe moving in the same direction, a figure closely tied to the gamma reversal as dealers scrambled to adjust their positioning.

Among the 500 highest-liquidity stocks, 69 hit their peak implied volatility on April 30, while 379 reached recent lows. That kind of gap between the most volatile names and everything else is a signature of speculation concentrated in specific corners of the market rather than distributed evenly.

Names flagged for unusual options activity include DKNG, RKT, EPD, TGT, and FTCH, a grab bag of sports betting, mortgage lending, energy infrastructure, retail, and fashion.

ZeroHedge described the situation as “unprecedented moves in correlation and dispersion” driven by speculation in “a handful of US names.”

Why this pattern has teeth

The most obvious parallel is the 2021 meme-stock frenzy, when gamma squeezes in GameStop and AMC turned options market structure into the primary driver of equity prices. The 2023 regional banking turmoil offers another reference point, where rapid gamma shifts coincided with outsized moves in bank stocks that caught most institutional investors off guard.

What this means for investors

For crypto market participants, the connection is less abstract than it might seem. Extreme gamma positioning in equities tends to suppress measured volatility, specifically the VIX, even as actual risk builds underneath. That suppressed vol environment is exactly when risk assets, including Bitcoin and major altcoins, tend to attract the most speculative capital.

The 86% breadth figure is impressive, but it is also fragile. When nearly everything moves in the same direction because of dealer mechanics rather than earnings or fundamentals, the reversal tends to be similarly uniform. Diversification benefits evaporate precisely when you need them.