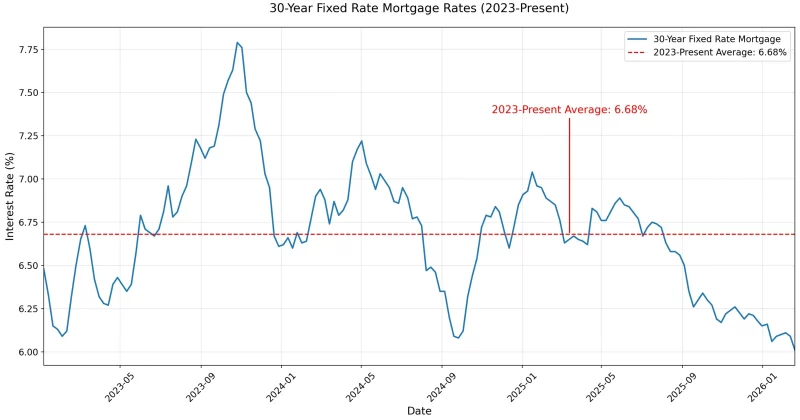

Freddie Mac reports 30-year fixed mortgage rate at 6.51%, highest since late August 2025

A 15-basis-point weekly jump signals growing affordability headwinds for homebuyers and a broader risk-appetite shift that crypto investors shouldn't ignore.

Borrowing money to buy a house just got more expensive. Again.

Freddie Mac’s Primary Mortgage Market Survey, released May 21, pegged the average 30-year fixed-rate mortgage at 6.51%. That’s up from 6.36% the prior week, a 15-basis-point jump that pushes the benchmark rate to its highest level since late August 2025.

For context, a year ago the same rate sat at 6.86%. So yes, rates are still lower year-over-year. But the direction of travel over recent weeks is the part that matters to anyone shopping for a home, refinancing existing debt, or trying to gauge where risk appetite is headed across financial markets.

The numbers and what they actually mean

The 15-year fixed-rate mortgage, a popular choice for refinancers and buyers who can stomach higher monthly payments, averaged 5.85% in the same survey. Both figures reflect conventional loans extended to borrowers with strong credit profiles and 20% down payments. In English: these are the rates the most creditworthy borrowers get. Everyone else pays more.

A 15-basis-point move in a single week might sound small. It is not. On a $400K loan, the difference between 6.36% and 6.51% translates to roughly $40 more per month in payments. Over 30 years, that adds up to more than $14,000 in additional interest.

Freddie Mac Chief Economist Sam Khater noted that potential buyers can offset some of the sting by shopping around. Comparing quotes from multiple lenders, he emphasized, can save borrowers significant money over the life of a loan.

Why mortgage rates keep grinding higher

Mortgage rates don’t move in a vacuum. They’re heavily influenced by yields on 10-year US Treasury bonds, which themselves respond to inflation expectations, Federal Reserve policy signals, and investor demand for safe-haven assets. When Treasury yields rise, mortgage rates tend to follow.

The late-August 2025 comparison point is telling. Rates touched similar levels back then before pulling back over the autumn months. Whether this current spike follows a similar pattern or represents the start of a more sustained move higher will depend largely on incoming economic data and Fed commentary over the next several weeks.

What this means for investors, including crypto

Higher borrowing costs reduce disposable income for millions of households. Less disposable income means less money flowing into discretionary investments. Crypto, for most retail participants, is still firmly in the discretionary bucket. When mortgage payments eat a bigger share of monthly budgets, the amount left over for risk assets tends to shrink.

Rates at 6.51% are still below the 6.86% level from a year ago. The danger scenario is a continued grind higher toward 7% or above, which would represent a more serious affordability crisis and a more meaningful headwind for risk assets.

For crypto investors specifically, the key variable to watch isn’t the mortgage rate itself. It’s what the rate tells you about the Fed’s likely path. If the bond market is right that rates stay higher for longer, the tailwind that crypto bulls have been counting on, namely a dovish pivot from the Fed, gets pushed further into the future.

The practical takeaway for anyone managing a portfolio that includes both real estate exposure and digital assets: the cost of capital is rising, and the market is telling you to plan accordingly. That might mean locking in rates sooner rather than later if you’re buying property, or simply acknowledging that the macro backdrop for speculative assets just got a little less friendly.