Nvidia plans to return roughly half its free cash flow to shareholders through buybacks and dividends

The AI chip giant is targeting about $48 billion in annual shareholder returns, a move that underscores just how much cash its GPU empire is printing.

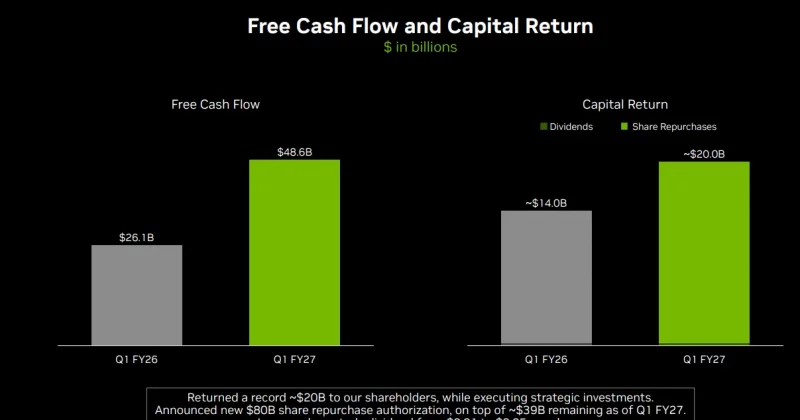

Nvidia is getting more generous with its cash pile. The company announced plans to return approximately 50% of its free cash flow to shareholders through a combination of stock buybacks and dividends, a significant escalation of its capital-return strategy that reflects the sheer volume of money flowing in from the AI boom.

With expected free cash flow of around $96.5 billion for fiscal year 2026, that 50% target translates to roughly $48 billion heading back to investors annually. To put that in perspective, that’s more than the entire market capitalization of most S&P 500 companies, returned to shareholders in a single year.

The numbers behind the policy shift

Nvidia has already been putting serious money to work on this front. In fiscal 2026, the company delivered approximately $40.1 billion in share buybacks alongside $974 million in dividends. The new 50% target suggests those figures are heading higher.

The buyback component is doing double duty here. Beyond simply returning cash to shareholders, repurchases have been helping offset the dilutive effect of stock-based compensation that Nvidia uses to attract and retain the engineering talent powering its AI chip development. Think of it as plugging a hole while filling the bucket: employee stock grants create new shares, buybacks take shares off the market.

The dividend piece, while relatively modest compared to the buyback program, signals something important about how Nvidia’s leadership views its cash generation. Companies don’t commit to sustained dividend payments unless they’re confident the money will keep coming. Dividends are sticky. Once you raise them, cutting them later sends a terrible signal to the market. Nvidia is essentially telling investors: we believe this revenue trajectory is durable.

Here’s the thing. A company returning half its free cash flow still gets to keep the other half. For Nvidia, that means roughly $48 billion annually to reinvest in R&D, expand manufacturing partnerships, and build out the next generation of AI hardware. It’s a both-and strategy, not an either-or.

Why this matters beyond the balance sheet

Capital return announcements from tech companies tend to mark inflection points. Apple’s massive buyback program, launched in 2012, signaled its transition from a high-growth disruptor to a mature cash-generating machine. Microsoft followed a similar arc. Nvidia making this kind of commitment now tells you something about where it sees itself in its own lifecycle.

That doesn’t mean growth is over. Far from it. Nvidia’s earnings have been on a record-breaking trajectory driven by insatiable demand for its GPUs across data centers, cloud providers, and AI startups. But the company is acknowledging that it generates more cash than it can efficiently reinvest, and rather than letting it sit on the balance sheet earning modest interest, it’s sending it back to the people who own the stock.

The timing is deliberate. Nvidia’s stock has experienced extraordinary appreciation over the past two years, and a more aggressive buyback program provides a price floor of sorts. When a company is spending tens of billions annually buying its own shares, that creates persistent demand in the open market. It doesn’t prevent declines, but it dampens them.

For institutional investors managing large positions, the buyback commitment also reduces a nagging concern: dilution. Tech companies are notorious for issuing generous stock compensation packages that quietly erode existing shareholders’ ownership stakes over time. Nvidia’s buybacks have been specifically designed to counteract this dynamic, and the new 50% target suggests the company wants to get ahead of it more aggressively.

What this means for investors

Look, Nvidia returning $48 billion to shareholders annually would make it one of the largest capital-return programs in corporate history. That kind of commitment tends to attract a different class of investor. Growth-oriented funds that bought Nvidia for its AI story will stay. But income-focused and value-oriented investors now have a reason to look more seriously at the stock, broadening its shareholder base and potentially reducing volatility over time.

The competitive landscape matters here too. Nvidia’s ability to return this much cash while still investing heavily in next-generation chips highlights the margin advantage it holds over rivals. Companies like AMD and Intel simply don’t have the free cash flow to simultaneously fund aggressive R&D and return tens of billions to shareholders. It’s a flex, financially speaking.

There are risks worth watching, though. The 50% target is based on current free cash flow projections, which assume continued dominance in AI chip sales. If demand softens, if hyperscalers develop more of their own silicon, or if export restrictions tighten further, that $96.5 billion cash flow estimate could come down. And a commitment to return half of a smaller number is a very different proposition.

The other thing to monitor is whether the buyback program is well-timed. Companies have a mixed track record of repurchasing shares at attractive prices. Buying back stock near all-time highs looks great if the stock keeps climbing, and looks wasteful if it doesn’t. Nvidia’s management is betting that its current valuation, even at these levels, represents a good use of capital compared to alternatives.

For crypto-native investors hoping this announcement might include some kind of Bitcoin treasury strategy or token-related initiative, there’s nothing here on that front. This is a straightforward, traditional capital-return play from a company that happens to be the most important hardware provider in the AI ecosystem.