Starlink generates over $11 billion in revenue for SpaceX, transforming it into a telecom giant

The satellite internet division now dwarfs SpaceX's rocket launch business, pulling in more annual revenue than many legacy telecom companies.

SpaceX’s satellite internet service Starlink has crossed $11 billion in revenue, a milestone that effectively completes the company’s metamorphosis from rocket builder to global telecom infrastructure provider. For context, that’s more annual revenue than companies like Dish Network, and it puts Starlink in the same revenue tier as some mid-cap publicly traded telecom firms.

The number is striking not just for its size, but for its velocity. Starlink’s revenue was estimated at roughly $7.5 to $8 billion in 2024, meaning the service appears to have grown by more than 50% year-over-year. That kind of growth rate is unusual for any business, let alone one that requires launching thousands of satellites into low-earth orbit.

How Starlink got to $11 billion

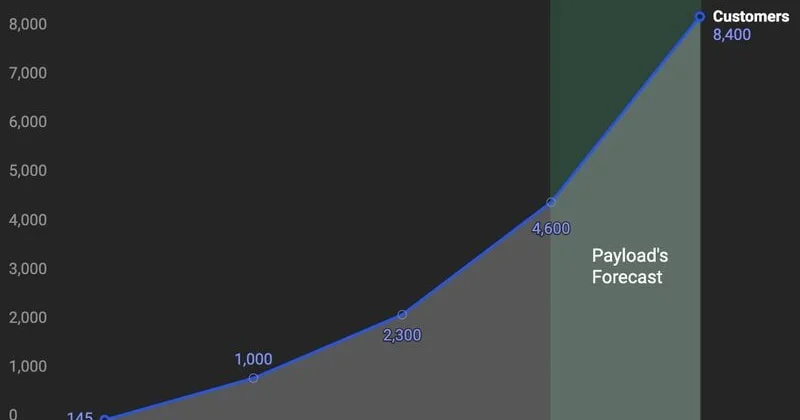

The math behind the milestone is relatively straightforward. Starlink has amassed approximately 10 million subscribers globally, each paying an average of around $92 per month. Multiply those numbers together and you land right in the $11 billion neighborhood.

But the consumer broadband business is only part of the story. Starlink has been aggressively expanding into enterprise and government contracts, which carry significantly higher price points than residential service. These contracts, which range from maritime connectivity to military communications, have boosted average revenue per user and diversified the customer base beyond rural homeowners who just want to stream Netflix without buffering.

The subscriber growth itself has been remarkable. Starlink launched its beta service in late 2020 with a modest number of users. Reaching 10 million subscribers in roughly four years makes it one of the fastest-scaling internet service providers in history. Traditional ISPs spent decades building out infrastructure to reach comparable customer bases, and they had the advantage of not needing to put their equipment in space.

Here’s the thing: Starlink’s growth trajectory doesn’t appear to be slowing down. Projections from multiple independent estimates suggest the service could hit approximately $15 billion in revenue by 2026. If those numbers hold, Starlink alone would be worth more than many standalone publicly traded companies.

SpaceX’s identity shift

For most of its existence, SpaceX was defined by its rockets. Falcon 9 launches, Starship development, NASA contracts. The launch business built the brand and the engineering credibility. But Starlink has quietly become the financial engine that powers everything else.

The revenue split tells the story clearly. When your satellite internet division generates more than $11 billion annually, it’s no longer a side project or a clever way to fill rocket payload capacity. It’s the main business. SpaceX’s launch services, while still significant and strategically important, are now the supporting act rather than the headliner.

This transformation matters for how SpaceX is valued in private markets. The company’s valuation, which has climbed steadily in recent secondary market transactions, increasingly reflects Starlink’s recurring revenue streams rather than the more episodic launch business. Recurring revenue from millions of subscribers is the kind of cash flow profile that makes investors salivate, and it provides the financial stability to fund ambitious projects like Starship and Mars colonization.

In English: SpaceX found a way to make its rocket launches pay for themselves by creating a massive telecom business that rides on top of those same rockets. It’s vertical integration taken to its logical extreme.

What this means for the competitive landscape

Starlink’s $11 billion revenue run isn’t happening in a vacuum. The low-earth orbit connectivity sector is heating up fast, and deep-pocketed competitors are making their moves.

Amazon has committed close to $35 billion to its competing Project Kuiper LEO satellite constellation. The e-commerce giant also acquired Globalstar in a deal worth $11 billion, signaling that it views satellite connectivity as a core strategic priority rather than an experimental bet. Apple, meanwhile, has been integrating satellite connectivity features into its iPhone lineup, creating another vector of competition in the direct-to-device segment.

The competitive dynamics create an interesting tension. Starlink has a massive first-mover advantage with thousands of satellites already in orbit and millions of paying customers. But Amazon’s willingness to spend tens of billions suggests this won’t be a one-player market for long. The question is whether Starlink can maintain its growth rate and market position as well-capitalized rivals begin deploying their own constellations.

For investors watching SpaceX in secondary markets, or positioning for a potential future IPO of Starlink as a standalone entity, the $11 billion figure serves as a crucial benchmark. Revenue growing at more than 50% annually for an infrastructure business is exceptional by any standard. The risk lies in whether that growth rate can persist as the subscriber base matures and competition intensifies.

The enterprise and government segments may prove to be the real differentiator going forward. Consumer broadband is a price-sensitive market where competitors can undercut on monthly fees. But military contracts, maritime connectivity, and aviation partnerships involve longer sales cycles, higher switching costs, and substantially fatter margins. Starlink’s early lead in securing these contracts could create a moat that’s harder for competitors to breach than simply matching consumer pricing.

Look, a satellite internet company generating $11 billion in annual revenue would have sounded like science fiction a decade ago. The fact that it’s now a baseline number, with $15 billion potentially on the horizon for 2026, suggests the satellite broadband market is still in its early innings despite Starlink’s enormous head start.