US manufacturing activity expands at fastest pace in four years as prices surge to uncomfortable levels

The ISM Manufacturing PMI climbed to 54.0 in May while input costs hit a four-year high, creating a complicated picture for the Fed and crypto markets alike.

US factories are humming again. Manufacturing activity grew at its fastest clip since mid-2022 in May, driven by a surge in new orders and production that blew past analyst expectations.

The catch: the cost of making all that stuff is rising fast too, with input prices hitting levels not seen in four years.

The numbers tell a complicated story

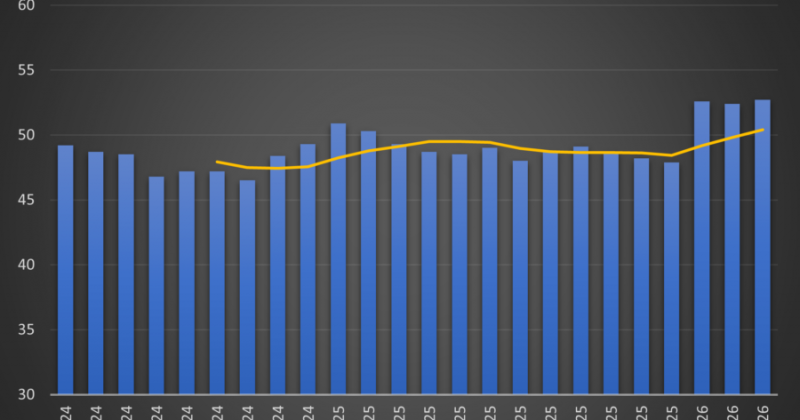

The S&P Global flash Manufacturing PMI jumped to 55.3 in May, comfortably above the 53.8 that analysts had penciled in. Anything above 50 signals expansion, so 55.3 represents genuinely strong territory.

The ISM Manufacturing PMI, the other widely watched gauge, climbed to 54.0 from 52.7 in April. Both readings point in the same direction: broad-based acceleration across the factory sector.

Dig into the sub-indices and the picture gets more interesting. The new orders index reached 56.8, suggesting demand is building rather than fading. Production hit 54.3, confirming that factories are responding to those orders with real output.

The prices-paid index, which tracks what manufacturers shell out for raw materials, surged to 84.6. That’s a four-year high.

From contraction to expansion in five months

To appreciate how dramatic this turnaround is, rewind to December 2025. The ISM index sat at 47.9, firmly in contraction territory.

The swing from 47.9 to 54.0 in roughly five months is notable. But the reasons behind the recovery deserve scrutiny, because not all of this growth may be organic.

A significant chunk of the recent PMI gains appears driven by defensive stockpiling. Companies have been hoarding raw materials to hedge against price volatility and potential shortages tied to tariffs. That stockpiling juices the PMI numbers in the short term. Purchasing activity goes up, inventories swell, and the headline figures look great. Once those inventories normalize, the artificial boost disappears.

Geopolitical tensions are amplifying the urgency. The ongoing conflict with Iran was cited in 42% of business responses as a factor influencing procurement decisions.

Despite all this increased output, manufacturing employment actually contracted, with 2,000 jobs lost in April. Factories are producing more with fewer people. This disconnect between output and employment suggests companies are leaning on automation, overtime, and efficiency gains rather than adding headcount.

What this means for crypto and risk assets

With the prices-paid index at 84.6, the Fed faces pressure to keep monetary policy tighter for longer. Higher-for-longer interest rates are historically a headwind for speculative assets, crypto included.

Bitcoin has historically attracted interest as an inflation hedge, and persistently elevated input costs could reinforce that narrative. If manufacturers keep paying more for materials and those costs flow through to consumer prices, the case for holding an asset with a fixed supply gets a little stronger.

The employment contraction adds another wrinkle. Strong output without hiring means consumer spending power isn’t growing at the same pace as production.

Watching whether new orders sustain above 55 in the coming months will be more telling than any single data point from May.