Bank of England holds rates at 3.75%, warns of ‘forceful’ hikes if inflation keeps climbing

Governor Bailey calls the decision an 'active hold' as Middle East conflict clouds the inflation outlook for the UK economy.

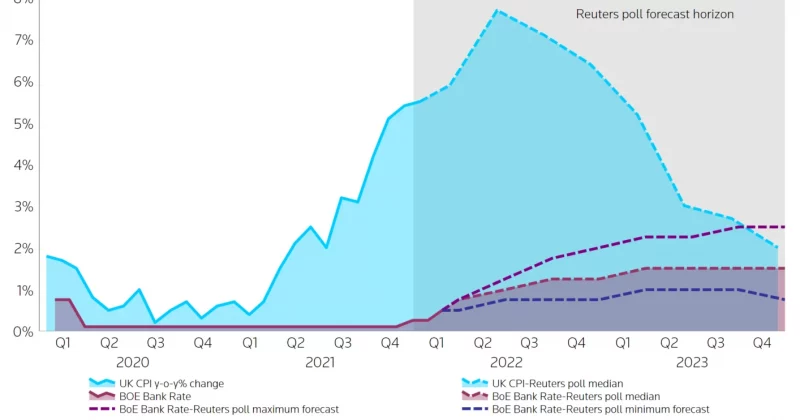

The Bank of England opted to keep its benchmark Bank Rate parked at 3.75% following its Monetary Policy Committee meeting on April 30, 2026. The vote was 8-1, with only one dissenter, Huw Pill, pushing for a quarter-point increase to 4%.

Governor Andrew Bailey went out of his way to frame this as something more deliberate than a shrug. He called it an “active hold,” a phrase designed to communicate that doing nothing was, in fact, doing something.

Why standing still counts as a stance

The Bank Rate sat at roughly 5.25% not that long ago, and the journey down to 3.75% reflected a period of deliberate monetary easing as inflation cooled. Bailey pointed to that prior tightening as evidence the bank has already taken significant action to address earlier economic shocks.

The ongoing conflict in the Middle East, particularly tensions linked to Iran, has thrown a wrench into energy markets. That’s feeding directly into inflation pressures just as policymakers thought they were getting the situation under control.

UK CPI inflation currently sits at 2.8%, which is only slightly above the BoE’s 2% target. But recent forecasts suggest it could climb to around 3.3%, which would represent a meaningful drift in the wrong direction.

Bailey acknowledged this directly. While the current policy position is restrictive, he made clear the bank is prepared to act with “forceful” rate increases if inflationary pressures keep building from sustained supply disruptions.

The balancing act between growth and prices

Bailey was explicit that the hold was influenced by what the bank is seeing in both activity data and labor market effects. The economy has already absorbed a lot of tightening, and the full impact of previous rate moves is still working through the system.

The lone dissenter, Huw Pill, apparently disagreed with that calculus. His vote for a 25-basis-point hike suggests at least some members of the committee believe the inflation risks from geopolitical disruption warrant preemptive action rather than watchful waiting.

The next MPC meeting is scheduled for June 18, 2026. Between now and then, energy prices and Middle East developments will likely dominate the committee’s inbox.