PBOC sets up offshore central bank repo facility to boost RMB liquidity

China's central bank expands tools for offshore institutions to access renminbi funding through enhanced repo operations

The People’s Bank of China is building new plumbing for the offshore renminbi market, setting up a facility designed to give foreign institutions better access to RMB liquidity through repurchase agreements.

What the PBOC is actually doing

The facility centers on repo operations, which are essentially short-term borrowing arrangements where institutions pledge collateral (in this case, RMB-denominated bonds) in exchange for cash. The PBOC has been working closely with the Hong Kong Monetary Authority on these enhancements. New measures announced in January 2025 enable offshore RMB repo transactions using Northbound Bond Connect holdings as collateral. Those operations are slated to begin in September 2025.

Bond Connect is the channel that lets foreign investors trade in mainland Chinese bond markets without needing separate onshore accounts. Using those bonds as repo collateral makes holdings that might otherwise just sit in a portfolio do double duty as a source of short-term funding.

The eligible participants list includes offshore central banks, international organizations, sovereign wealth funds, and qualified foreign institutional investors.

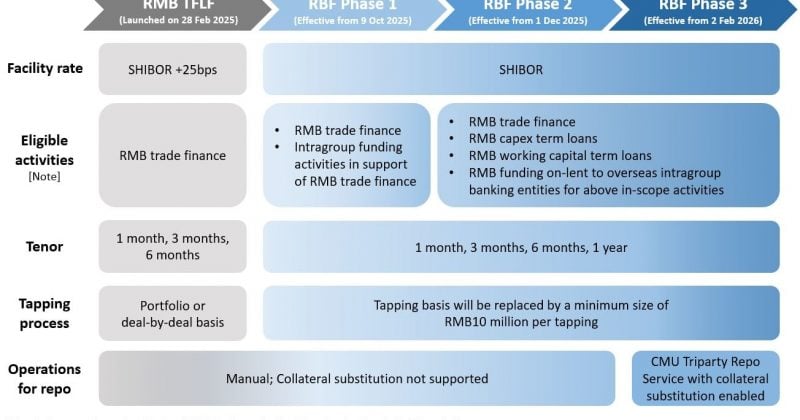

The PBOC has also been enhancing the HKMA’s RMB Liquidity Facility, originally established in 2012, with improvements extending through early 2026. Alongside that sits the RMB Business Facility, backed by PBOC currency swap lines, which is similarly being expanded with a particular focus on cross-boundary and offshore repo transactions.

Hong Kong as the RMB hub

Offshore RMB deposits in Hong Kong have surpassed RMB 1 trillion as of early 2026, reflecting the resilience supported by recent liquidity facilities.

The PBOC has also been issuing CNH bills in Hong Kong since the 2020-2021 period, providing an additional liquidity management tool for the offshore market. These instruments come with tenors ranging from overnight to several months.

What this means for investors

For institutional investors, the immediate practical impact is straightforward: better access to RMB liquidity means lower friction and potentially reduced funding costs when operating in yuan-denominated markets. If you’re a sovereign wealth fund holding Chinese government bonds through Bond Connect, you can now more easily use those bonds to raise short-term cash without selling the underlying position.

For the crypto and digital asset space specifically, the research found no direct connection between these repo facility enhancements and any digital asset initiatives.

Capital controls remain in place on the mainland, and the offshore market still operates within guardrails set by Beijing. Whether the repo facility meaningfully changes behavior among foreign institutional investors will depend on the terms, the collateral haircuts, and how smoothly the September 2025 launch actually goes.