FCoin Exchange Now Compared To Ponzi Scheme

FCoin has rapidly become the most (in)famous exchange in the market. Is the trans-mining model real and sustainable, or a Ponzi scheme?

Move over, Kitties. There’s a new clog in the Ethereum pipes, and this one’s not getting cleared anytime soon. Over the past weeks, FCoin has moved from an unknown back corner to the most (in)famous exchange in the market, with a volume that—supposedly— exceeds top coin marts like OkEx and Binance.

Here’s a quick reprise: the FCoin Exchange, which launched a bit over a month ago, runs on a unique business proposition: all transaction fees are reimbursed to the users, in the form of the exchange’s native Token. 51% of the FCoin Token supply is locked up and can only be extracted through trading, in a system the white paper calls “Transaction-fee mining” or “Trans-mining.”

Why Buy when You Can Sell to Yourself?

The system raised plenty of eyebrows as a slightly roundabout way of getting users funds. “You pay transaction fees to the platform with BTC and ETH,” said Binance’s Changpeng Zhao. “Then the platform pays ‘100%’ back to you with its token. Isn’t it just buying platform token with BTC and ETH? How is this different from an ICO?”

On Weibo, Zhao (who, unlike FCoin, does not pretend to give away crypto) predicted that the system would invite even more sleight-of-price than usual:

“If an exchange doesn’t get revenue from transaction fees and solely profits from the price of its token. How would it survive without manipulating the token price? Are you sure you want to play against a price manipulator? The same price manipulator who controls the trading platform?“

And, as expected, the FCoin order book appears to be crawling with bots. “The price of FT is constantly manipulated,” wrote one Redditor, who also described the exchange as a scam. It’s impossible to confirm who’s at either end of the trades, but a quick glance at the order book suggests that they’re not all human.

Manipulation hasn’t stopped other exchanges from taking notice and following suit. Coinbene and news when they briefly soared to the top of CoinMarketCap. Another exchange, BigONE, later joined in and currently sits on just under a billion dollars of daily trades. If you’ve never heard of any of those exchanges, that should give you a good idea who’s trading those huge volumes.

Coinbene, however, went one step further: repaying users with more money than they put in:

https://twitter.com/coinbene/status/1010167349582823425

Ethereum Stop Sign

But the real jimmy-rustler is the way new coins are listed. Instead of asking for money (like HitBTC) or having a contest (Kucoin), FCoin chose a very dramatic system for listing new entrants: one deposit, one vote.

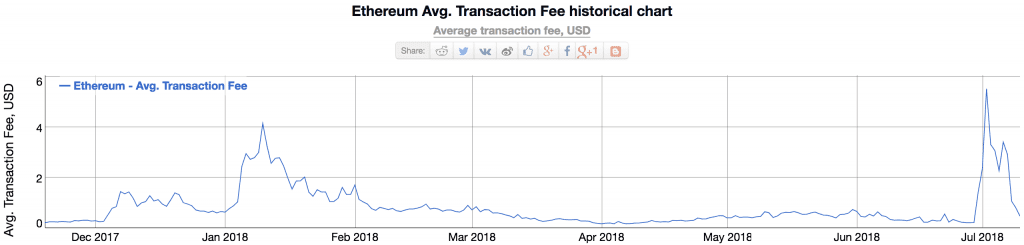

The result was a bit like those publicity stunts where someone organizes a flash mob in the middle of a busy highway. Given the way most coins jump at even a minor listing, it’s no surprise that the Ethereum network halted as a parade of minor ERC-20s and crypto-droppings swamped the doors. Gas fees swelled from under $0.10 per transaction, on average, to over five dollars.

This system is not inherent to Trans-fee Mining, and FCoin could have easily listed coins in a way that doesn’t upset the network. But the listing system does reflect the the exchanges’ priorities: it’s no surprise that a business that apparently welcomes wash trading would also bring its fake-looking volume onto the blockchain.

Welcome to Paradise

Then there’s the other features, which—compared to regular exchanges, look downright Utopian. Not only does the token entitle users to a share of the revenue stream (including Bitcoin and Ethereum income as well as FT), it also allows hodlers “to participate in business decisions, team elections and so on.”

Other exchanges have rewards programs, but FCoin is the only one that claims to return 80% to the users.

These are pretty big promises, and right now there are two likely scenarios:

- FCoin is attempting to become an online socialist commonwealth which shares profits, and in which the community votes on important decisions; or

- Trans-fee mining is an elaborate way of exchanging large quantities of Bitcoin and Ethereum (which cost quite a bit to make) for FCoin tokens, which cost the exchange absolutely nothing to create.

As much as we love decentralized governance and smart contract voting, cryptocurrency is not an environment in which every actor can be trusted to be pusuing the common good.

Accidentally Ponzed

All this talk of ERC-20s and smart contracts can get confusing, so here’s a quick analogy:

- Imagine a restaurant that’s technically free–whenever you buy a burger, you get reimbursed in coupons worth the price you paid

- At the end of the night, 80% of the cash register is redistributed among the coupon holders

- Since new customers are constantly coming in and buying burgers, some customers are able to “make 5% a day” in returns.

It doesn’t take a blockchain scientist to realize that for this restaurant to function, those coupons cannot be worth their face value.

Trans-fee Mining is a new model, and not everyone is impressed: the model has been described as a ‘Ponzi Scheme’ by some commentators, while others are threatening a class action lawsuit. It may be unintentional, but FCoin essentially seems to be repaying old customers with new money.

FCoin isn’t the first exchange to reward traders in its native token, but no one else has done so so extravagantly.

As much as we love complaining about the fees on Coinbase or Binance, at least we know how much we’re paying.

When an exchange promises your money back, and more, only a fool fails to recognize that the model is questionable, at best.

The author is invested in Bitcoin and Ethereum.