The Weird and Wonderful Relationship Between Crypto Market Cap and Volume

Why is a token with less than $1M traded per day a top-25 crypto asset?

The relationship between a coin’s market cap and its volume is not linear. This is where cryptocurrency markets differ from traditional stock markets, which have clearer tendencies toward a correlation. The immaturity of the cryptocurrency market and the inefficiencies of the current exchange model are likely at the heart of the discrepancy: but the centralization of crypto assets in a few ‘rich’ wallets is also hard to ignore.

The Volume to Market Cap Ratio

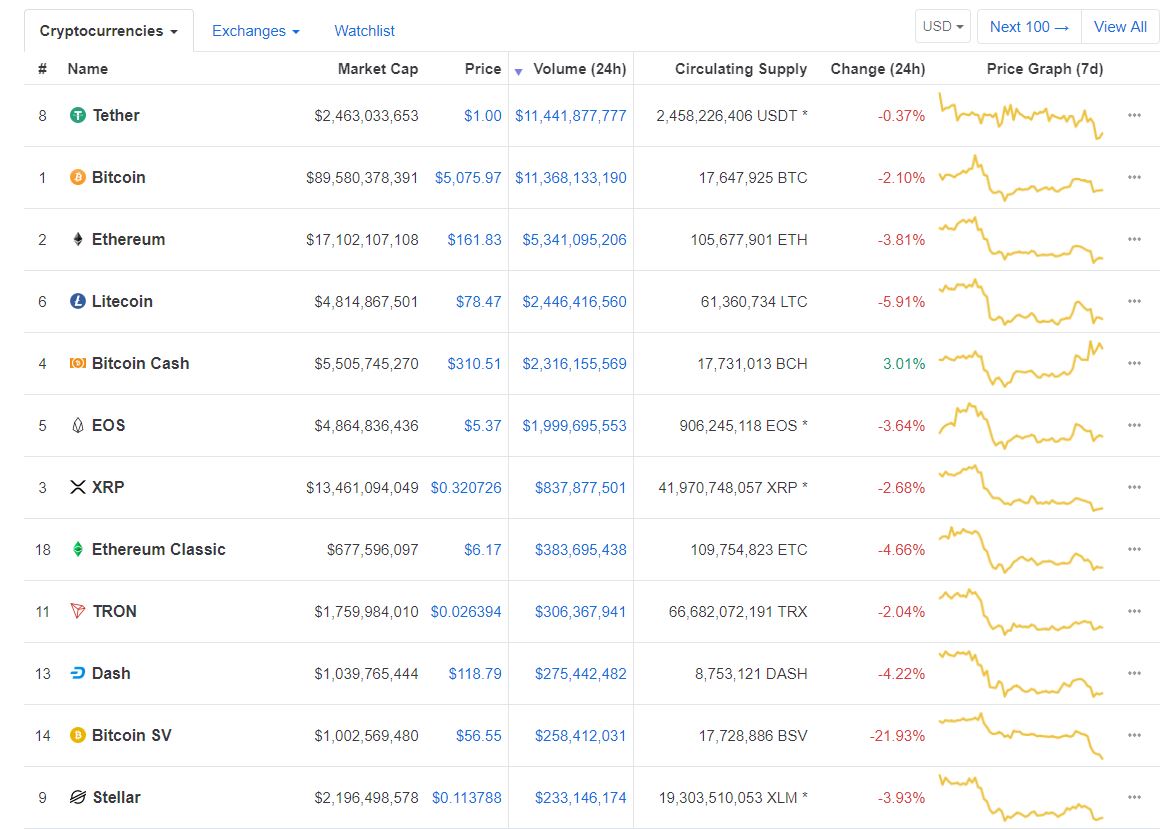

It’s intuitive to imagine that the larger a coin’s market cap, the more volume traded in any given period of time. But an interesting thing happens when you organize Coinmarketcap to view cryptos ranked by 24-hour trading volume.

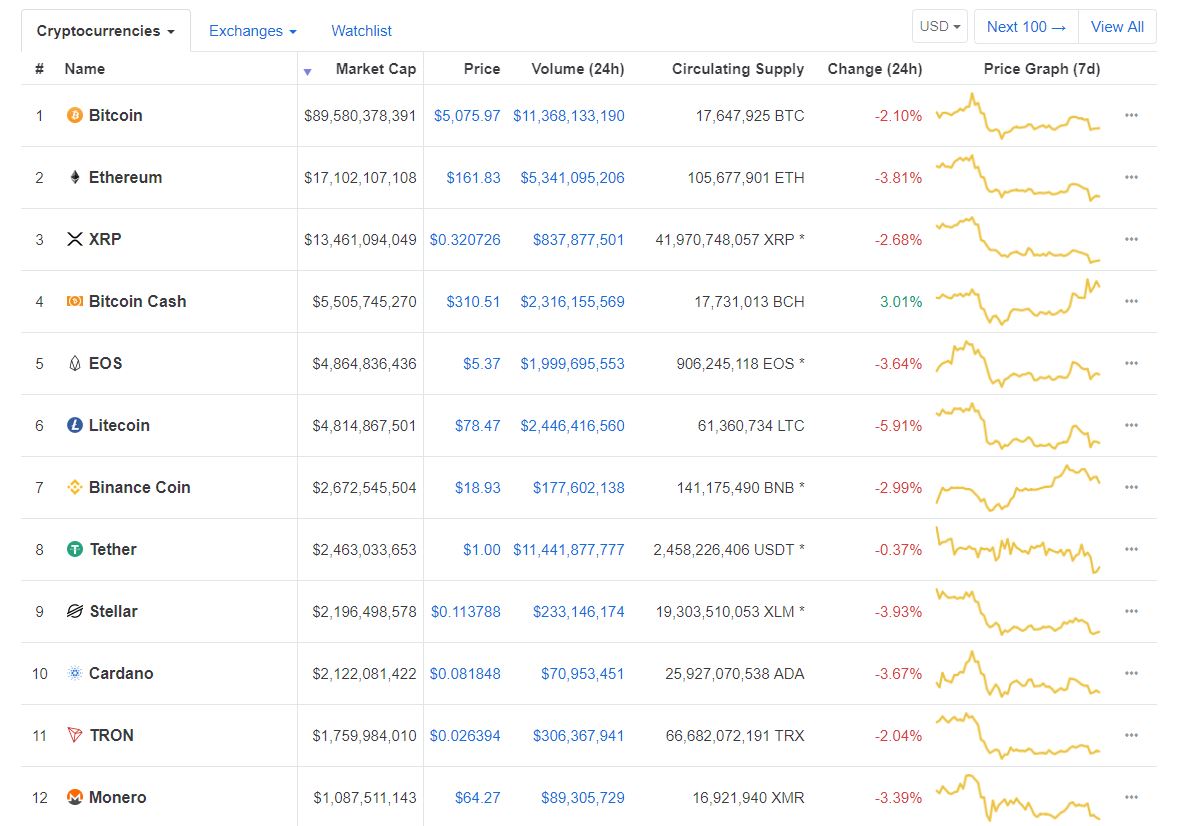

At the time of writing, for example, tether USDT has had the most volume traded in US dollar terms over a 24-hour period, followed by bitcoin, ether, litecoin, bitcoin cash (the Roger Ver version), and EOS. These seem an intuitive top six. XRP aside, they are among the top six coins in terms of market cap.

Tether, with the 8th highest market cap at around $2.5 billion, is widely traded both as an on-ramp coin from fiat and a safe haven stablecoin (although how safe it actually is has been open to debate for a long time).

The surprise omission from the top six in terms of volume is probably Binance’s native BNB. Many trades are paid for with BNB on the world’s top exchange by volume, so one might imagine its volume would be high. It came in at 15th in terms of 24-hour volume.

The Outliers

There are a number of outliers, though, when one compares market cap to trading volume. Tezos has a market cap just under $700 million. Its daily volume at the time of writing was a mere $6 million. ZCash, with a cap around $430 million, had a whopping 24-hour trading volume around $220 million – nearly half its market cap.

True USD and Paxos, both stablecoins, are ranked 36 and 60, respectively, in terms of market cap, but come in at 18 and 21 when it comes to volume. The explanation for those disparities are obvious: as stablecoins, one can imagine traders using them to trade into and out of to take advantage of price fluctuations in the market.

As for Crypto.com Chain – the market cap is currently listed by CMC as $427M. That’s based on a fully-diluted extrapolation. The total supply is 100 billion tokens, of which just over 5 billion are circulating; so even though the volume is listed at a meager $976K over the last 24 hours, the token manages to crack the top 25 because it has a price of around $0.08. In this regard, the metrics driving the measure of market cap are also occasionally questionable (although CMC did confirm to Crypto Briefing that they are under review).

When we examine NASDAQ daily volumes, Apple, Microsoft, and AMD were among the most actively traded stocks at press time, and they’re also among the index’s most valuable companies. Lyft was also heavily traded, and there is an explanation to that: it is a hyped stock at the moment, having very recently listed in a high-profile IPO. Among all US exchanges, daily liquidity is high among large companies: General Electric, Ford, and Bank of America feature among the most actively traded stocks.

The correlation between market cap and volume in traditional markets is not exactly linear, but it has always been quite intuitive. Smaller caps, especially lower profile stocks, tend to enjoy less liquidity than larger caps. That correlation doesn’t quite work in the crypto markets, and there are a number of reasons why.

Market Inefficiencies

Coins that do not trade on the larger exchanges are likely to enjoy less volume than those that do, regardless of their market capitalization. Tezos, for example, does not trade on any of the eight largest exchanges.

The largest exchange on which it does trade is Huobi, the world’s ninth largest. But that accounts for slightly above three percent of its volume. 22 percent of tezzies are traded on BitMax, the 50th largest exchange in the world by adjusted volume. Fewer buyers are likely to be tempted to trade a coin they cannot easily dispose of. The seemingly-endless distribution of crypto exchanges is one of the market’s many inefficiencies.

And there are some who argue that market cap, while not entirely meaningless, is a less useful indicator than it might first appear.

Concentration of Ownership And An Immature Market

Where there is a high concentration of ownership of a coin by whales who do not actually trade a coin actively but hold them, that coin’s liquidity is going to suffer. According to Bloomberg, about a thousand people hold 40 percent of the circulating supply of bitcoin, with the largest 100 wallets holding close to 20 percent of all bitcoin.

It is likely that a lot of that bitcoin is going to sit inactively in wallets and not shuffle around on a daily basis on exchanges. This is why, despite having Bitcoin having 45 times the market cap of USDT, tether punches above its weight in terms of volume.

Of course, that level of centralization is evident in plenty of other cryptos: Litecoin’s top 10 wallets hold 8.8% of all LTC, Dash is at 6.5%, and newer entrants to the market often have even more lopsided ownership – Groestlcoin, for example, may have 62,000 wallets, but the top 10 own 42% of the tokens.

Many of the apparent incongruities in relationships between indicators in crypto markets are the result of the immaturity of the market and the highly-dispersed nature of crypto exchanges.

Expect a more intuitive alignment between liquidity and market cap when the market matures. Until that time, unexpected relationships will persist.

Disclosure: The author was an early stage investor in Lyft.