IRS Makes Answering the “Yes or No” Bitcoin Question Much Easier

American tax authorities have added further clarification as to how investors should be reporting their crypto activity. And like traditional tax filings, failing to follow these instructions could spell trouble for users.

In a new move to ensure cryptocurrency tax compliance in the US, the Internal Revenue Service (IRS) has released additional draft instructions for filing tax returns.

How to Answer the IRS’ “Yes” or “No” Question

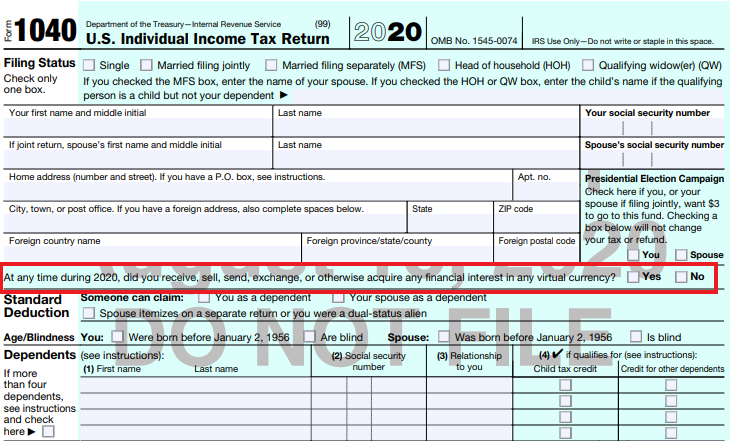

In the 2020 draft tax form (Form 1040), the IRS in September introduced a simple “yes” or “no” question regarding cryptocurrency transactions on the first page. Form 1040 is used to file federal personal income tax returns by US residents.

As per the draft’s instructions, those who sold cryptocurrencies, received airdrops, exchanged cryptocurrencies for goods, services, and other assets must report “yes” to the question.

The question in the draft Form 1040 reads as follows:

“At any time during 2020, did you receive, sell, send, exchange, or otherwise acquire any financial interest in any virtual currency?”

The IRS and other US agencies refer to cryptocurrencies as virtual currencies and define them as assets that are readily convertible to fiat money but are not legal tender. Before the latest announcement, there was still ambiguity about what “acquiring a financial interest in virtual currency” meant precisely.

The IRS now reports that a transaction involving virtual currency includes:

- The receipt or transfer of virtual currency for free, including from an airdrop or hard fork;

- An exchange of virtual currency for goods or services;

- A sale of virtual currency; and

- An exchange of virtual currency for other property, including for another virtual currency.

According to the IRS, users who held crypto in their wallets or transferred cryptocurrencies between their own wallets are not liable.

The draft instructions on Form 1040 are likely to be considered final unless unexpected issues require further changes.