Are CDPs the New CDOs?

By offering asset management, borrowing, lending, and remittance services DeFi is shaking up the traditional financial services industry.

DeFi Boom Becomes Dangerous as CDPs Trigger Memories of CDOs

DeFi has become a flagship use case for blockchain technology. By offering asset management, borrowing, lending, and remittance services without intermediary parties, DeFi is moving to shake up the traditional financial services industry. However, the increasing popularization of leverage instruments threatens the health of the market.

Investors in traditional markets still remember the horrors of the 2007 US housing market crash, and the subsequent financial crisis that followed. The debt crisis, as it was also called, was catalyzed by people overleveraging. On the ground, retail investors were caught up in the house-flipping frenzy; people were taking out mortgages that they could not pay off with the hope of flipping them at a profit.

Additionally, the financial industry created derivative instruments, known as collateral debt obligations (CDOs), that were supposed to provide revenue streams based on mortgage payments. Everything worked great while the real estate market was liquid and growing. When the music finally stopped and people could no longer resell these houses and therefore had no means of paying off their mortgages, the real estate market collapsed, taking the CDOs — and the institutions investing in them — with it.

The Makings of a Crypto Credit Bubble

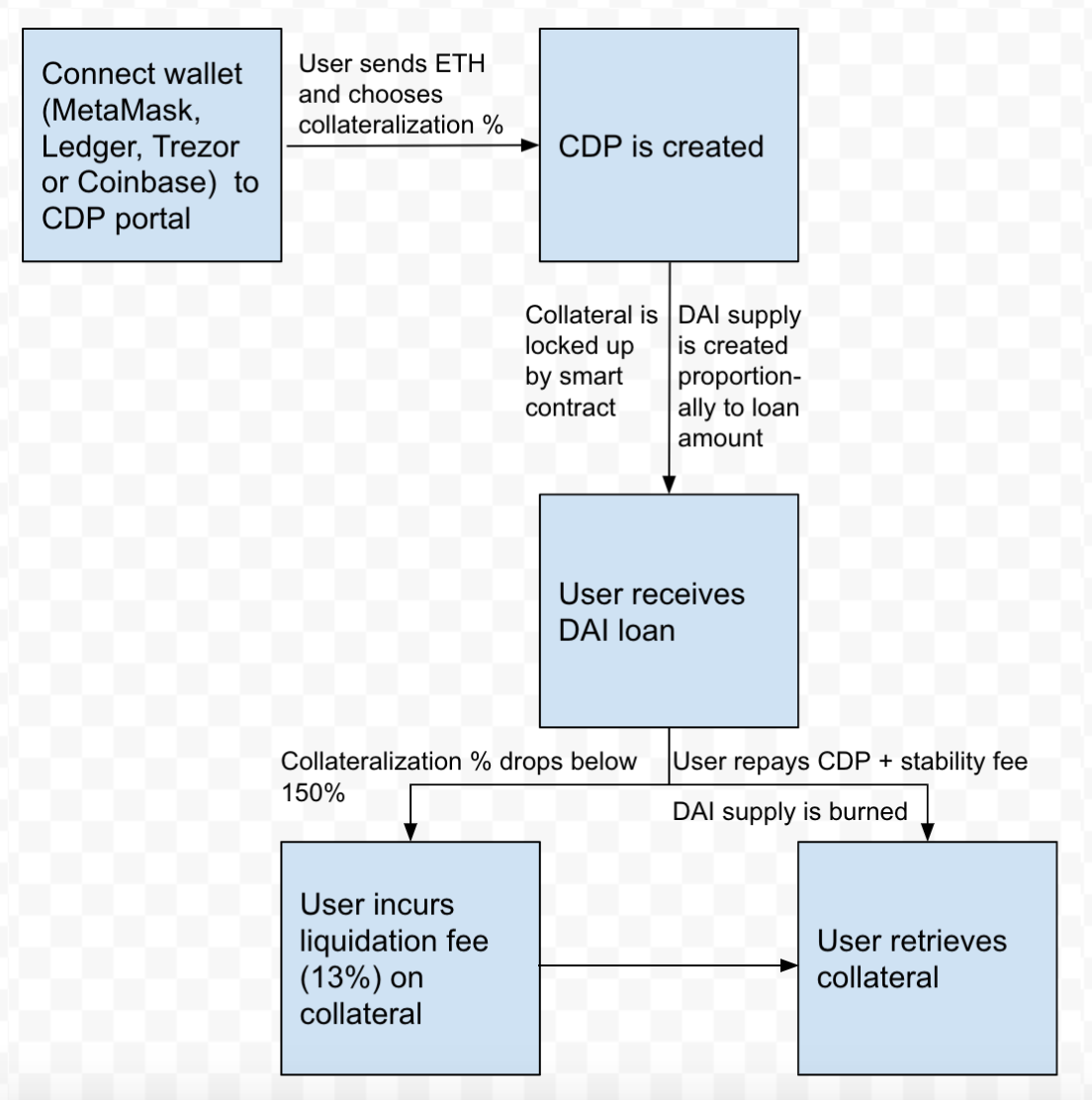

Crypto markets don’t have CDOs, but they do have CDPs, or collateral debt positions. This instrument, popularized by MakerDAO, enables users to take out loans using collateral assets. In the case of MakerDAO, this means leaving ETH in a smart contract as collateral and securing a loan in Sai (formerly Dai) a stable currency.

At face value, this is a great concept. Users can get loans quickly, and the initial value of the collateral is some multiple of the value of the Sai. So, if the market takes a turn for the worse, the collateral can be liquidated to ensure solvency. In the worst-case scenario, the governance token MKR is used for rescue buying.

However, there is an underlying assumption that there are use cases for Dai, otherwise users are just paying interest for no reason. Crypto-based use cases, like the integration in Augur, may be promising, but there are few applications that can generate enough demand for transacting in a coin that requires interest payments.

Additionally, everyday transaction demand may be growing. When strapped for cash, users who believe in the future value of Ethereum may not want to liquidate, and can opt for a loan. Integrations like the one with Monolith that make Dai available on debit cards, make closing short term budget gaps easier.

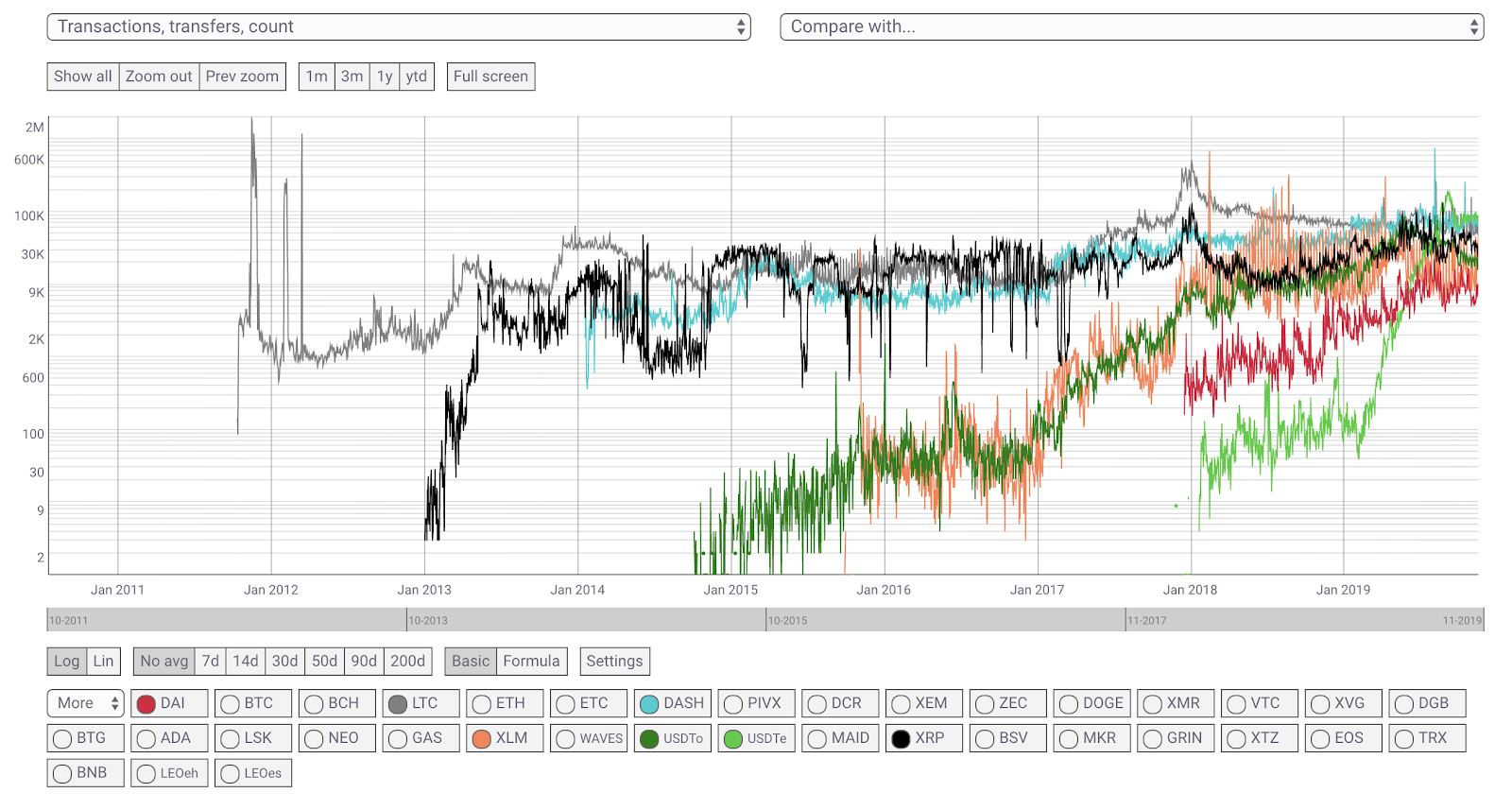

However, when compared to other digital currency projects, both stable and not, Dai shows a concerningly low transfer transaction count.

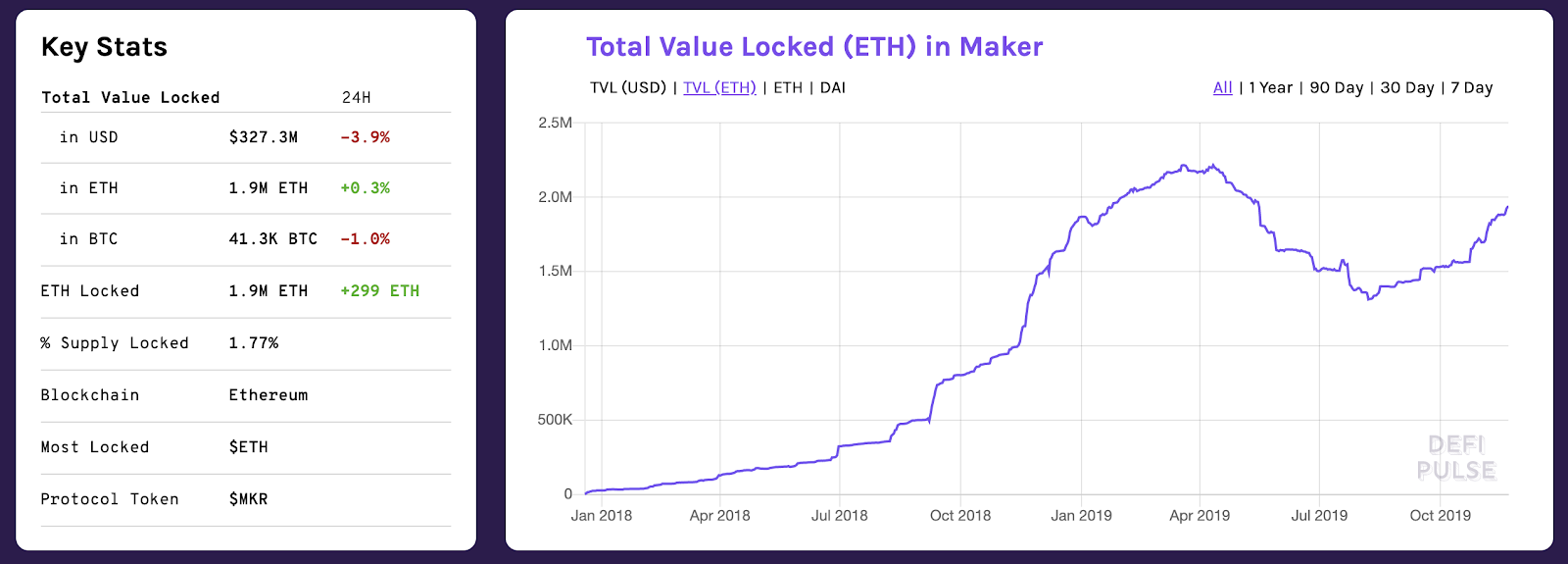

This leaves leveraging as the most exciting use case. Investors who want to speculate on Ethereum’s price increase can lock up their existing Ethereum and use Dai to purchase more Ethereum, even on margin. Not surprisingly, the Total Value (ETH) locked up in MakerDAO has grown throughout the crypto winter, and, despite a noticeable dip this spring, has been on an uptrend since late summer.

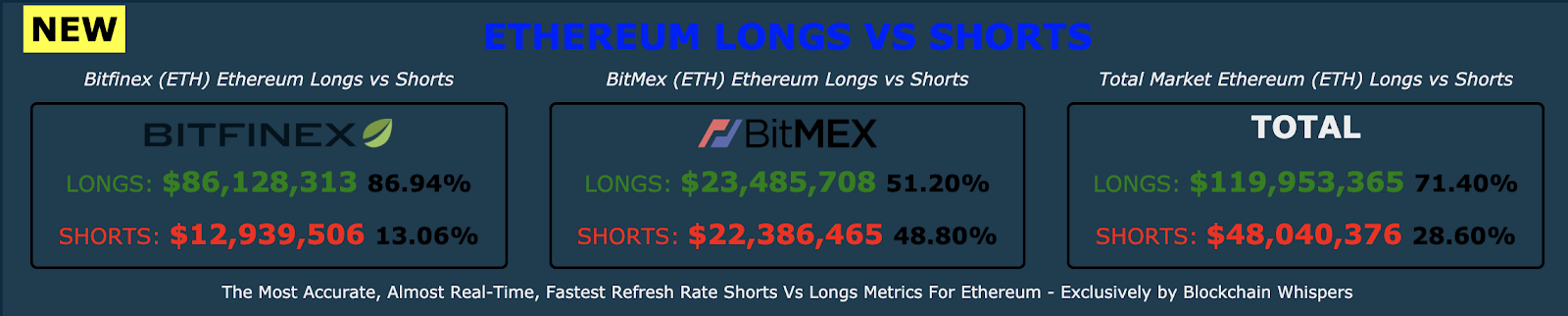

The idea is also supported by high long vs short ratio for ETH in the market.

Complexity That Can Lead to Calamity

As a result of this layering, we have a market that has ETH used as collateral for ETH bought on margin. Moreover, investors in MakerDAO actually buy and sell MKR, which is not directly tied to the CDPs. If that sounds overly complicated and dangerous, it is.

Moreover, we are at risk of a dangerous “bad news is good news” pattern developing. For those who believe that ETH prices are bound to go up, downward movements in the price of the asset may appear as solid buying opportunities.

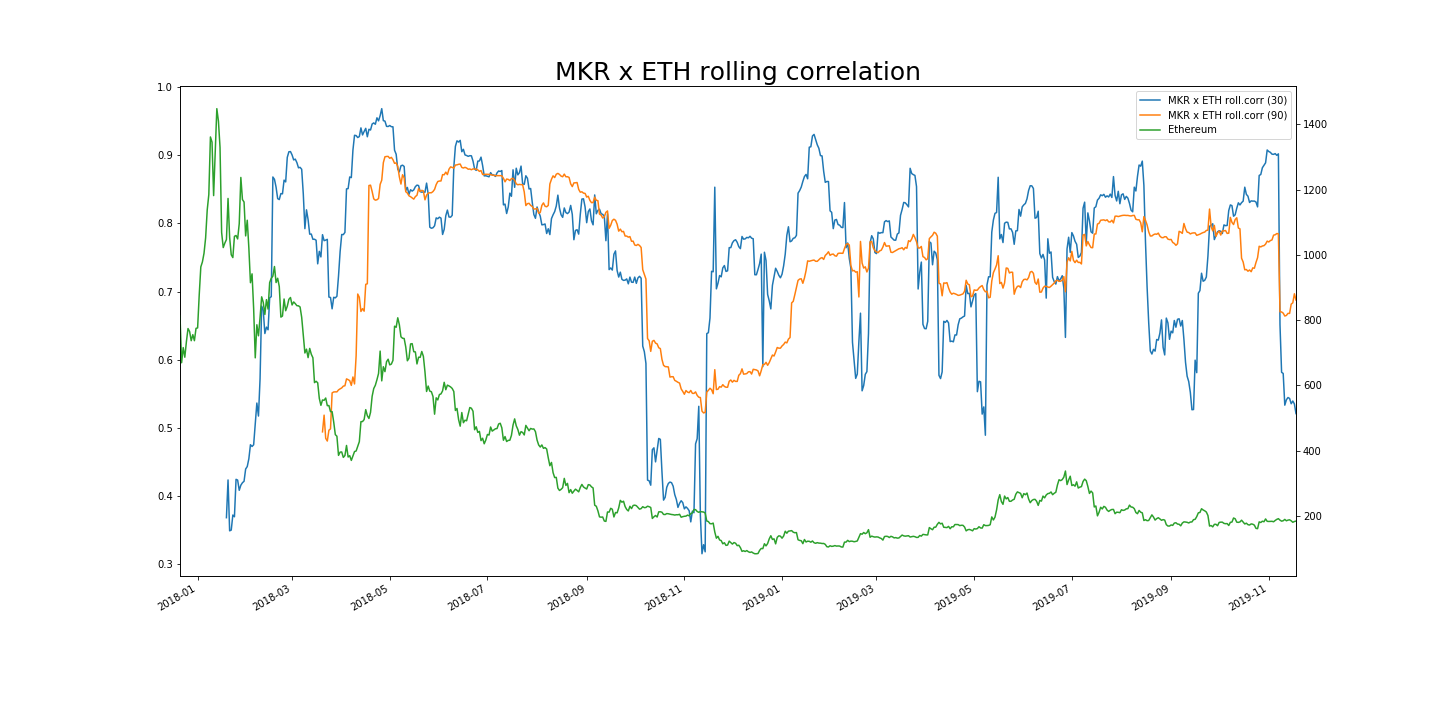

The periodic divergences in the correlation of MKR and ETH may indicate that MKR is looking to decouple from the collateral asset ETH.

As the Number of Assets Grows, so Does the Bubble

MakerDAO’s recent upgrade allows users to collateralize loans with assets other than ETH. Basic Attention Token will be the first token enabled, but others may follow. So, if the Sai for ETH on margin trends grows, the market is likely to see an abundance of of risk profile mismatches.

One of the critical flaws of the CDOs was the bundling of assets with different risk profiles and misrepresed combined risk.

The developing trend around leveraged assets in crypto may be following the same pattern. Moreover, retail investors in MKR often don’t understand the utility function of the token and the risks involved in the system as a whole.

Now Kava intends to spread the model outside the Ethereum ecosystem by offering cross-chain leverage products. These should usher in the era of CDPs with BTC and other non-Ethereum tokens as collateral.

The Big Short

The industry is gearing up for more leveraging, with few participants understanding the mechanisms and the potential downside. As the leverage bubble grows and more institutional investors enter, it will only be a matter of time before a big short begins to make sense. If enough ETH is traded on leverage with ETH as collateral (this works with other assets too), a large enough short can cause both a massive margin call event and the liquidation of the CDP collateral. The combined effect of the two could be devastating for the industry as a whole. The prospects of what this could do if replicated with BTC are even more concerning.

The crypto industry is nowhere big enough to have the same impact on the global economy as that of the credit bubble in the traditional markets. So, if the CDP-margin trading system implodes, we are not likely to see a “Big Crypto Short” movie, but there may nevertheless be drama.

For now, there does not appear to be an immediate threat, as the DeFi space has not yet grown to be systemically important for the industry. The road ahead is filled with growth and expansion for the sector, but it is important to raise critical issues early so they may be addressed at a fundamental level. DeFi should play an important role in the future of the global economy, but the lessons of traditional markets should not be ignored.

Disclaimer: The author(s) of this article is/are invested in the following coins: Bitcoin.