DeFi Lending Could Undermine Security of Proof-of-Stake

The rise of DeFi and the threat to network security

Lending and borrowing crypto, a subset of DeFi applications, has quickly boomed into an almost billion-dollar industry. But does it pose a threat to Proof of Stake networks?

The DeFi landscape includes lending protocols, security tokens, derivatives, and exchanges, and threatens to usurp traditional financial models into trustless protocols that leverage decentralized networks.

The Rise and Rise of DeFi

Ethereum’s DeFi ecosystem is easily the most significant, with the original smart contract platform host to several DeFi applications. As Alex Pack from Dragonfly Capital told Forbes, “The goal of DeFi is to reconstruct the banking system for the whole world in this open, permissionless way. You only get that shot every 50 years.”

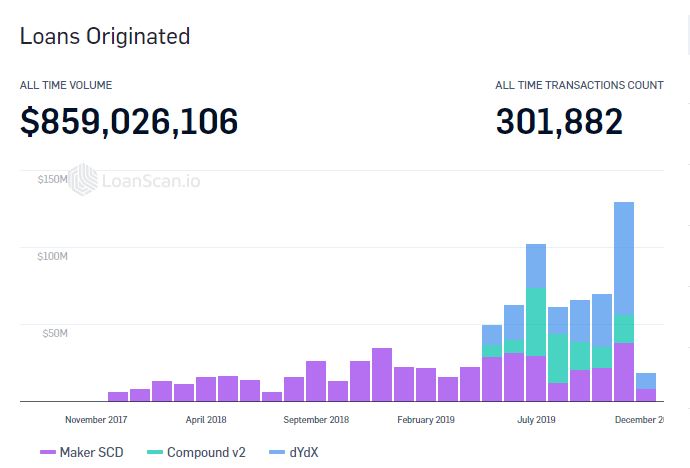

The popularity of crypto lending markets has skyrocketed over the past two years. Bloqboard, which recently rebranded as the Linen App, says DeFi’s “core principles are transparency, accessibility and financial inclusion.” The company highlighted that active outstanding loans on four open lending protocols—MakerDAO, Dharma, dYdX, and Compound Finance—rose 1,200 percent in 2018 to reach as high as $72 million.

Speculators may use Maker to bet on the long-term price appreciation of Ether, for example, by putting up Ether as collateral, creating stablecoin DAI (for the cost of an interest rate), and using that DAI to purchase more Ether.

But typical lending and borrowing traders in crypto are being used to access cash without selling the underlying crypto asset, which is used as collateral. According to Loan Scan, since the end of 2017, loans originated through decentralized finance applications amount to roughly $850 million.

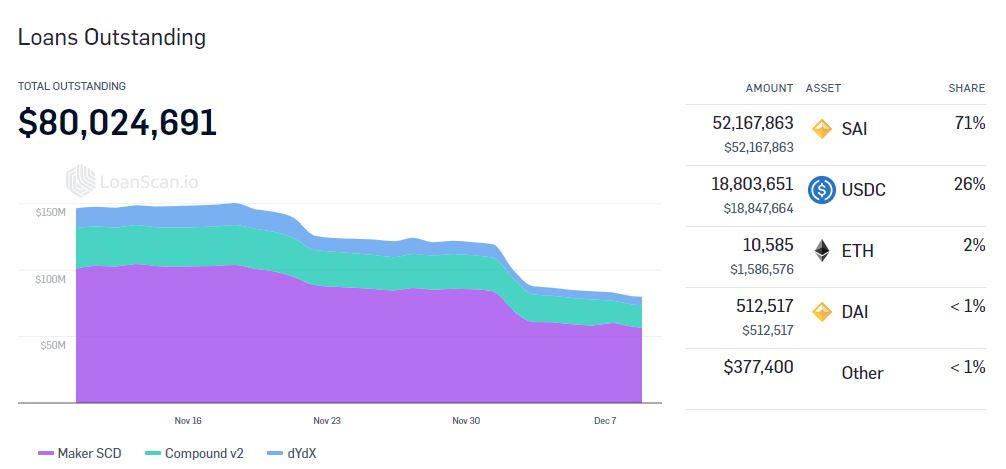

Over 80 percent of these loans have been in SAI, the previous single collateral version of DAI, which is borrowed against Ether as collateral. There is currently $80 million worth of total DeFi loans outstanding. The figures pale in comparison to the cryptocurrency market’s total capitalization of around $200 billion. But for any given network, DeFi contracts could prove destructive.

The market cap of Ether, for example, is roughly $16 billion. With 80 percent (almost $700 million worth) of crypto loans originated being in SAI, collateralized by Ether, almost 5 percent of the Ether supply is connected to SAI lending markets. According to Forbes, as of April this year, “Two percent of all ether, or about $339 million worth of ether, is locked up in Dai. Compound has about $34 million in locked ether, while Dharma has roughly $10 million.” Compound is a crypto money market issuer.

With SAI and DAI so prominent in these figures, there is a possibility that lending will become more rewarding than staking as Ethereum moves from PoW to PoS, potentially threatening its security, as well as all other PoS networks.

PoS Network Security Relies on Staking Rewards

In most PoS algorithms, two-thirds of all staked assets need to be owned by honest actors to ensure the security of the network. But what could happen if yields from lending become more attractive than those for staking? Rational stakers would stop staking and start lending.

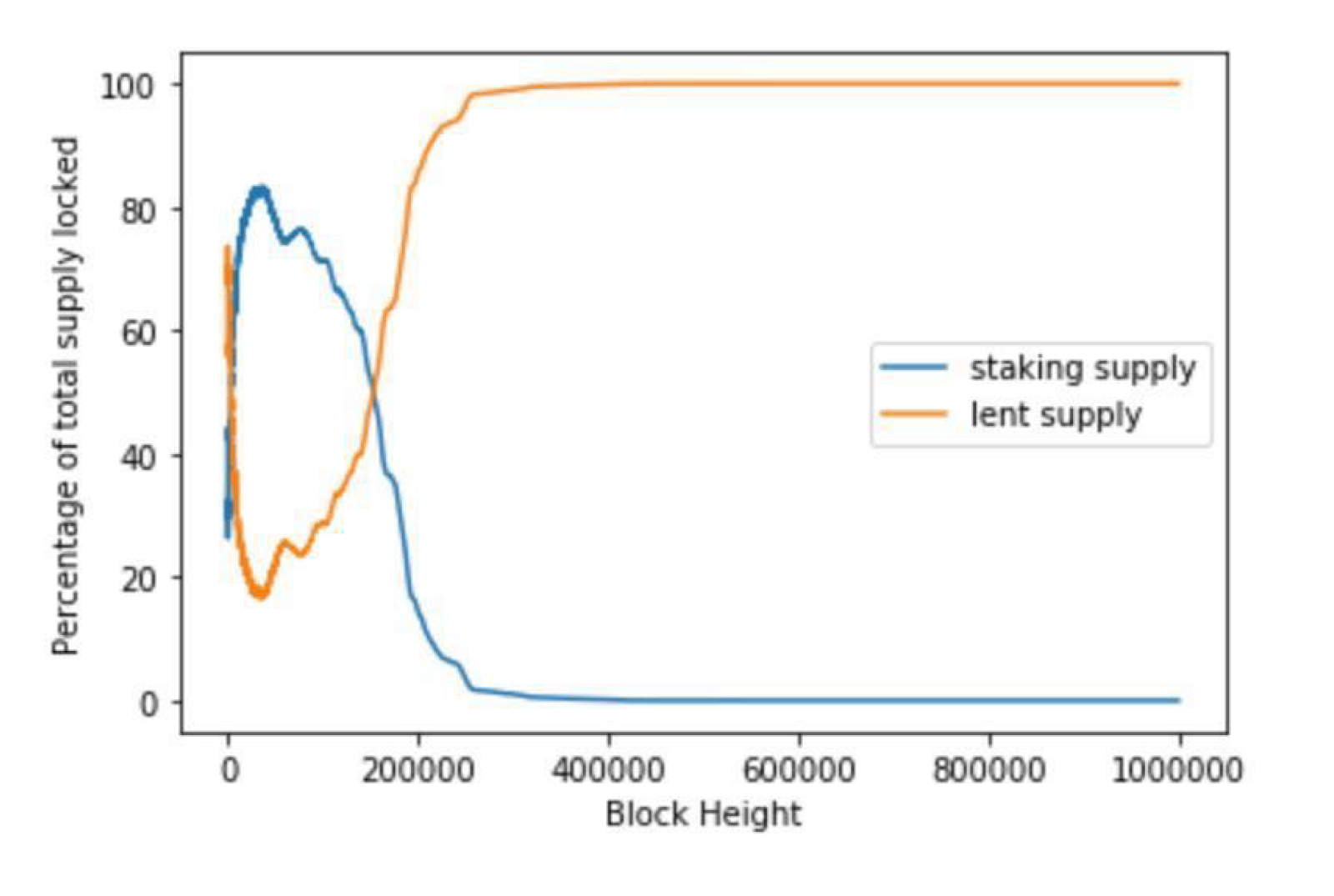

Tarun Chitra from Gauntlet calculated what he termed the ‘Competitive equilibria between staking and on-chain lending,’ in which he analyzed the interaction between PoS staking and on-chain lending. Chitra found that “High lending yields would likely lead to a reduction in network security as these yields would encourage rational actors to unexpectedly coordinate and reduce network security by optimizing for financial gain.”

Graphically, assuming Bitcoin-style deflationary block rewards, the pivot from staking to lending on the Ethereum network would look like this:

The implications are stark. Proof of Stake networks cannot safely reduce block rewards because doing so would encourage stakers to switch to lending. The pivot point would be that at which staking was less lucrative than lending. If block rewards were to fall continuously, the incentive to lend instead of staking would stay indefinitely.

Exposure to Attack

If block rewards on PoS networks do fall in this manner, the network will always be susceptible to attackers using collateral to borrow through smart contracts. By increasing borrowing demand, they will increase the interest rate.

Once the interest rate hits the point at which it exceeds the rewards from staking, it will have the effect of attracting staked coins into the borrowing market — reducing the number of staked tokens.

The twin knock-on effects of this are that as the number of tokens staked falls, traders may short the underlying asset due to its fading security, causing downward price pressure. Secondly, as more and more stakers abandon it for lending, a malicious actor could purchase a large number of tokens, stake them, and undermine the security of the network.

The implications for Proof of Stake chains are clear. Their security relies on inflationary tokenomic models. Without a continued level of incentives to stake tokens and help secure the network, the rewards from lending will erode interest in staking.

In deflationary models with falling block rewards, “on-chain lending smart contracts can cannibalize network security in PoS systems.” Tokenomic design becomes critical. Incentives to stake must always ensure that on-chain lending contracts cannot switch the balance in favor of lending over staking. PoS networks must deploy inflationary models to protect their own security.