A Comparison of DeFi Protocol Token Valuations

A PE model for valuing DeFi tokens

The proliferation of DeFi protocols was the crypto story of last year. But how do the major token valuations compare?

Valuing DeFi Protocol Tokens

DeFi protocols earn money by charging usage fees. The fees are distributed to token holders in the form of earnings or through burns that reduce the supply of tokens. Earnings generate a direct return to participants in the market while burning tokens increases each users’ relative share of the network.

Lucas Campbell from DeFi Rate proposed a price-to-earnings (PE) ratio to determine the value of the competing DeFi network and protocol tokens. Campbell drew data from Token Terminal, a data outfit focused on crypto, to draw his narrative.

By comparing network earnings to token price, investors are able to compare which tokens are valued appropriately.

Price-to-earnings ratios are used in traditional investment products to obtain a snapshot valuation of an asset. The ratio compares share prices to the underlying earnings of the company. It is a measure of how many years the company would take to earn the equivalent of its market cap.

PE ratios are simple measures to compare companies with each other and to examine a company’s performance in light of its historical performance. A PE ratio in the DeFi token market can be expressed as market cap divided by annualized earnings.

This obtains a price-to-earnings multiple that reflects the fairness of token pricing.

Given how new the DeFi economy is, the PE ratio may prove to be an unreliable metric. But when compared across tokens in the DeFi market, it is at least useful in determining how attractively priced each token is.

The lower the PE ratio, the better priced the token is. It can also mean the higher the expectation is that future income flows will decline, all other things being equal.

DeFi Token Earnings

Different DeFi tokens have different earnings models that complicate PE calculations. These differences need to be accounted for to derive meaningful metrics. Some of the different fee distribution models are outlined below.

The spread between the Dai Savings Rate (DSR) and the Stability Fee (interest paid by borrowers) is used to burn MakerDAO (MKR) tokens. On the Synthetix protocol, SNX holders stake tokens to earn fees created during the exchange of Synths.

Uniswap does not have tokens. The trading fees generated on the platform are distributed to the liquidity providers in the liquidity pools. Kyber Network charges users exchange fees, which are payable in KNC tokens. Some of the tokens are burned and some of them are distributed to KNC stakers.

Nexus Mutual is a decentralized insurance protocol used to insure users against software bugs or hacks. Nexus’ unique system boosts the price of the NXM token by adding the Ether and DAI used to purchase coverage to the capital pool once the coverage expires.

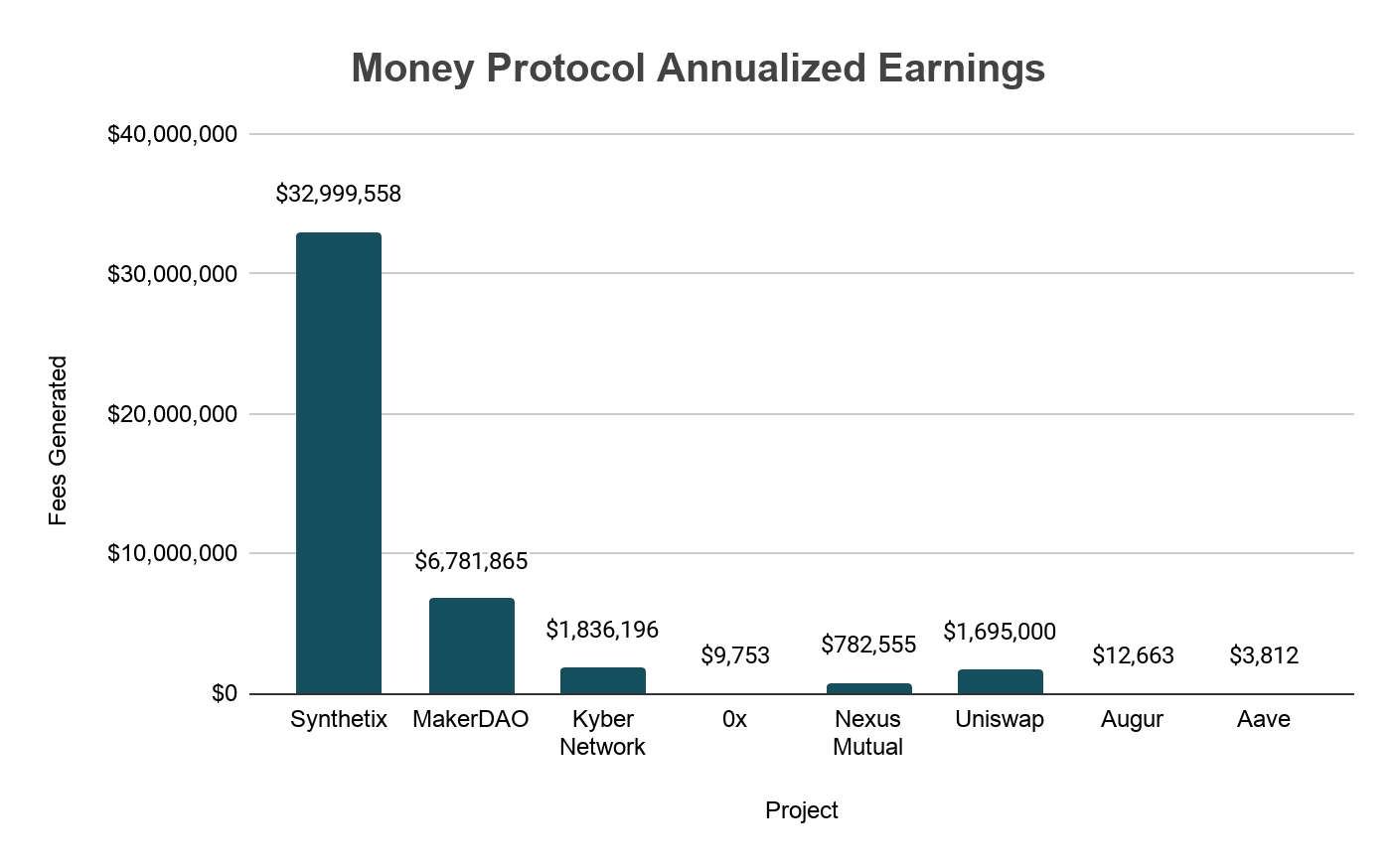

Earnings among these major protocols, aggregated by Token Terminal, are summarized in the graph below:

Synthetix’s earnings substantially outstrip those of MakerDAO, despite the latter’s dominance in the market. Maker dominance, according to DeFi Pulse, is currently at 74%. Synthetix has annualized cash flows of around $32 million collected from the 0.3% fees on Synth trades.

MakerDAO has annualized earnings of around $6.7 million from the spread between the Dai Savings Rate and the Stability Fee. Kyber Network and Uniswap, both permissionless liquidity protocols, are the only other two platforms to produce meaningful returns, at just under $2 million each.

Nexus Mutual returns less than $1 million in annualized earnings.

PE Ratios Compared

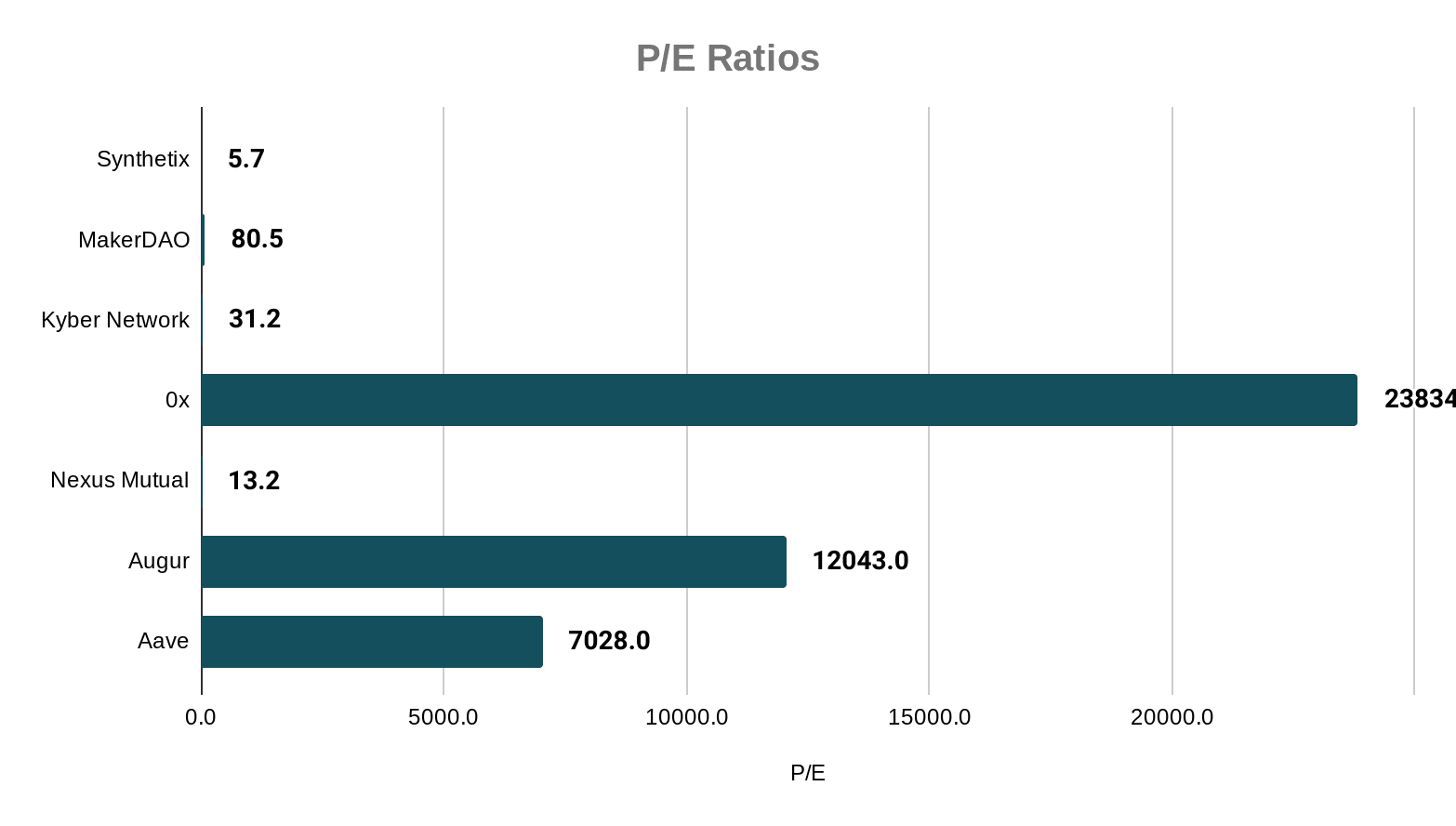

Dividing the respective market capitalization of the DeFi protocols above by their annualized earnings, the following PE ratios are calculated:

As the graph depicts, MakerDAO has a high PE ratio of around 80. Kyber Network’s PE ratio is slightly above 30. Nexus Mutual’s PE ratio, at about 13, is similar to the long-term average PE ratio observed in traditional equity markets.

For reference, the S&P 500 has a long-term average PE ratio of 15. Shares are priced at around 15 times annual earnings. In tech and other high growth stocks, those ratios tend to run much higher. Nasdaq’s average PE ratio is almost 33. Alphabet’s PE ratio is currently around that level.

Synthetix has a low PE ratio at under six. By potential high growth sector standards, both Synthetix and Nexus Mutual could be said to be potentially undervalued at their current PE ratios. Kyber Network, the on-chain liquidity protocol that recorded explosive growth at the beginning of the year, has a PE ratio that appears to value it fairly if measured against traditional tech company valuations.

Augur, Aave, and Ox, also listed here, have price-to-earnings multiples that are at absurd values.

They also have very little traction in terms of earnings. The figures reflect either one of two things: investors see growth trajectories that have yet to materialize or their tokens are manifestly overpriced. Over time, which is true will become clearer.

MakerDAO appears overpriced, but its PE ratio may accurately reflect its dominance in the market and its high growth potential. DeFi is such a new sector, that normalized PE ratios may take time to eventuate.

At current prices, the major projects mentioned above appear to be relatively healthy in terms of valuation levels.