Why Is XRP Crashing? Data Shows Ripple Is Flooding the Market

While the broader crypto market enjoyed a swift rebound from March lows, XRP prices continue to struggle. There’s not enough demand to absorb the tokens that Ripple is dumping on retail investors.

Ripple, and its XRP token, is one of the oldest projects in the cryptocurrency space, forming in 2012. Ripple’s value proposition was appealing to banks and settlement systems—offering to increase efficiency and cut costs with their solution.

The company’s token, XRP, boasted low fees and fast transaction times, placing the altcoin in direct competition with expensive and slow incumbents like Bitcoin. Despite these advantages, the coin has still failed to generate traction so far.

Leading Layer 1 platforms like Ethereum host a multitude of projects aimed at various audiences, from investors to RPG players. Implementing Decentralized Autonomous Organizations, or DAOs, is already a norm, and thanks to projects like Chainlink, blockchains can easily integrate with the outside world, financial institutions included.

By today’s standards, XRP Ledger (XRPL) has limited capabilities, which gets in the way of adoption among retail users. Institutional clients aren’t eager to use XRP for transactions, either, and holding it on their balance sheets is questionable given regulatory uncertainties surrounding the token.

It’s now evident that XRP’s benefits are unclear. Meanwhile, the XRP circulating supply continues to grow steadily, creating downward price pressure. This dynamic will continue until Ripple finds a way to grow the XRPL user base.

Blockchain, Not XRP

Ripple has set its sights on entering the lucrative payments market. This industry involves banks, payment processors, and remittance providers, each of which has sizeable expenses for moving money around the globe.

The usual process for transferring funds is slow, which can be problematic for unstable fiat currencies. To get around this, companies keep accounts in different countries with prepositioned liquidity. Once a sender sends money, a receiver gets the same amount minus fees from their local liquidity pool, so there is no need to carry physical cash.

Ripple’s principal value proposition is to provide a fast and cost-effective blockchain complete with a cryptocurrency to relieve companies from keeping large amounts of idle capital. The project’s On-Demand Liquidity (ODL) platform enables the transfer and conversion of currencies “in seconds.”

ODL is the part of the more extensive RippleNet network that gathers over 200 banking and financial partners. Besides ODL, RippleNet offers xCurrent and xVia blockchain-based payment systems that don’t use XRP.

While RippleNetwork has quite a few partners, it has created very little demand for the XRP token. There is at least one company trying to use the technology—MoneyGram, which Ripple purchased a sizeable equity stake in back in August 2019.

MoneyGram is a major ODL user, and regularly receives XRP from Ripple to facilitate the platform’s development, but the company sells tokens almost immediately because of regulatory concerns. Other large companies in RippleNet, like PNC, are not using XRP at all.

More than that, it wouldn’t make much sense to warehouse substantial amounts of XRP even if they did. The value proposition of using the coin for cross-border settlement is that it frees up idle capital. There would be no advantage in converting this liquidity to XRP and locking it up again.

The potential catalyst for the growth of XRP adoption among institutional clients is the possible acquisition of MoneyGram by Westen Union. The acquisition would transfer MoneyGram’s Ripple-technology agreements to Western Union, which could then become a significant XRP user.

Western Union’s CEO has, however, mentioned that the company’s settlement system is already quite efficient. Moreover, the company’s official position favors blockchain technology rather than cryptocurrency.

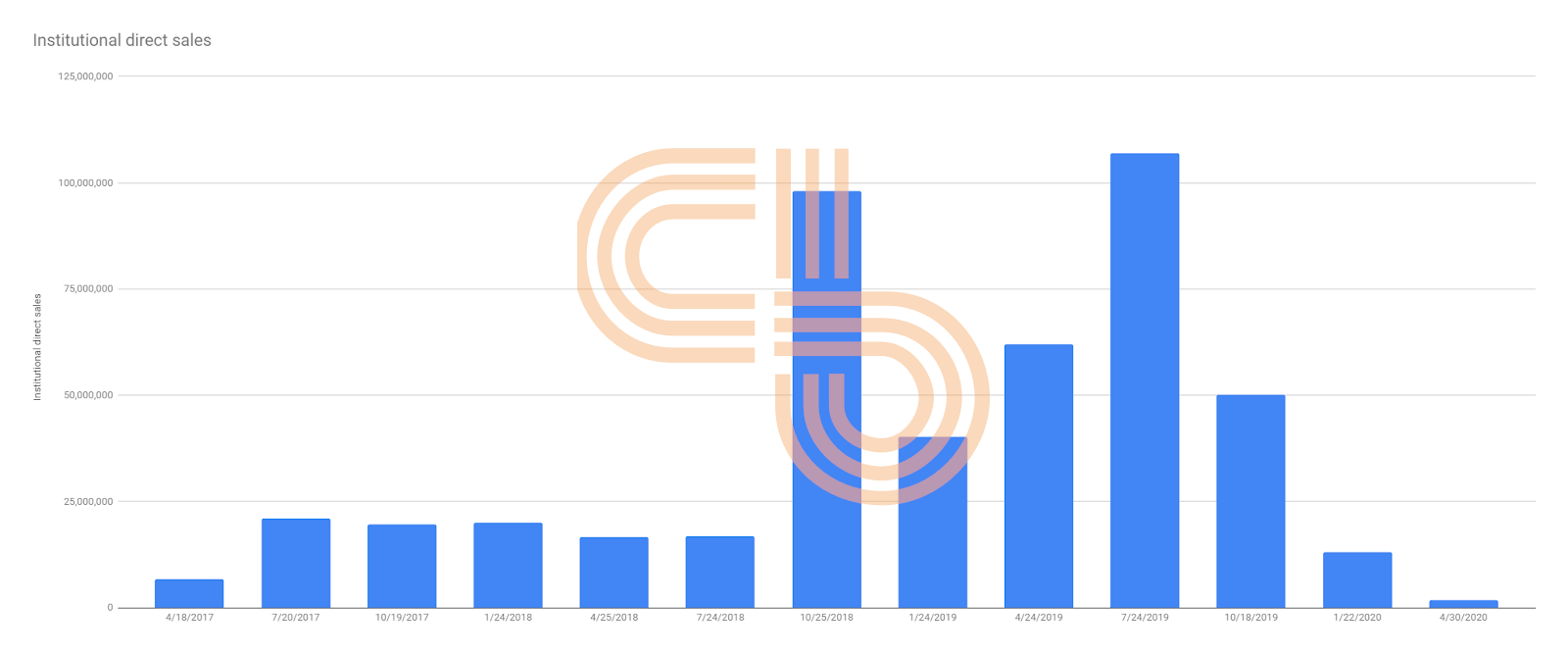

Overall, Ripple struggles to find institutional demand for XRP, which shows through declining institutional direct sales. Despite falling demand, Ripple has unlocked 300 million XRP (0.3% of the total supply) each quarter, eating-up whatever demand remains.

Ripple Is Losing Retail Investors

Without smart contracts, Ripple is inadequate for the needs of the market. It cannot offer capabilities beyond transacting XRP and issuing pegged tokens. Meanwhile, decentralized applications (dApps) and decentralized finance (DeFi) have caught the attention of the market, sucking up liquidity.

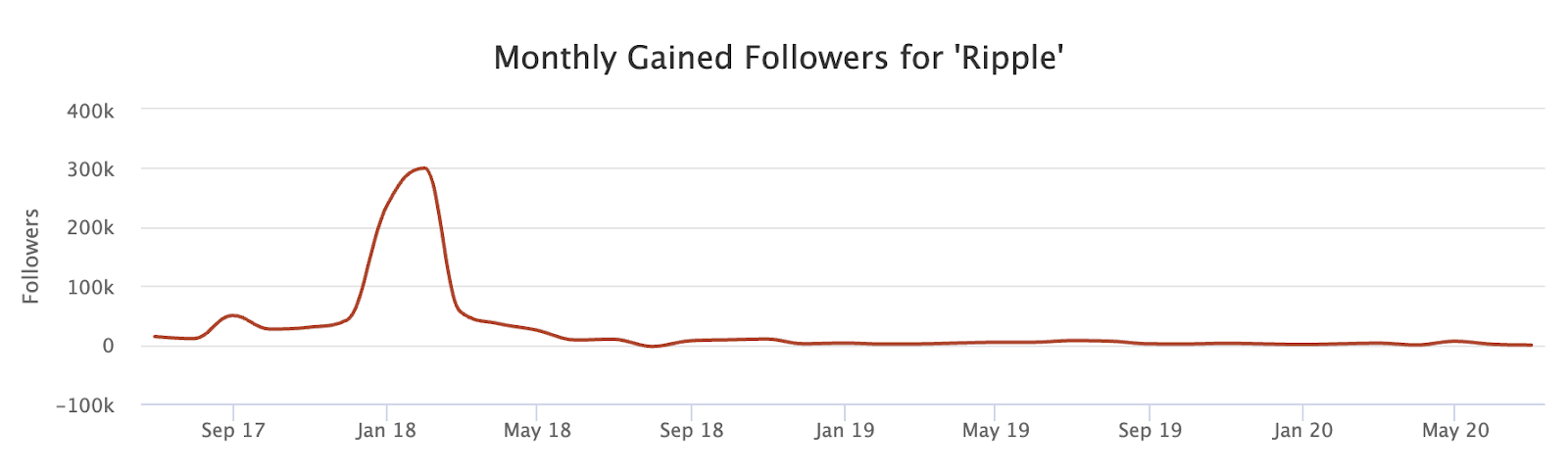

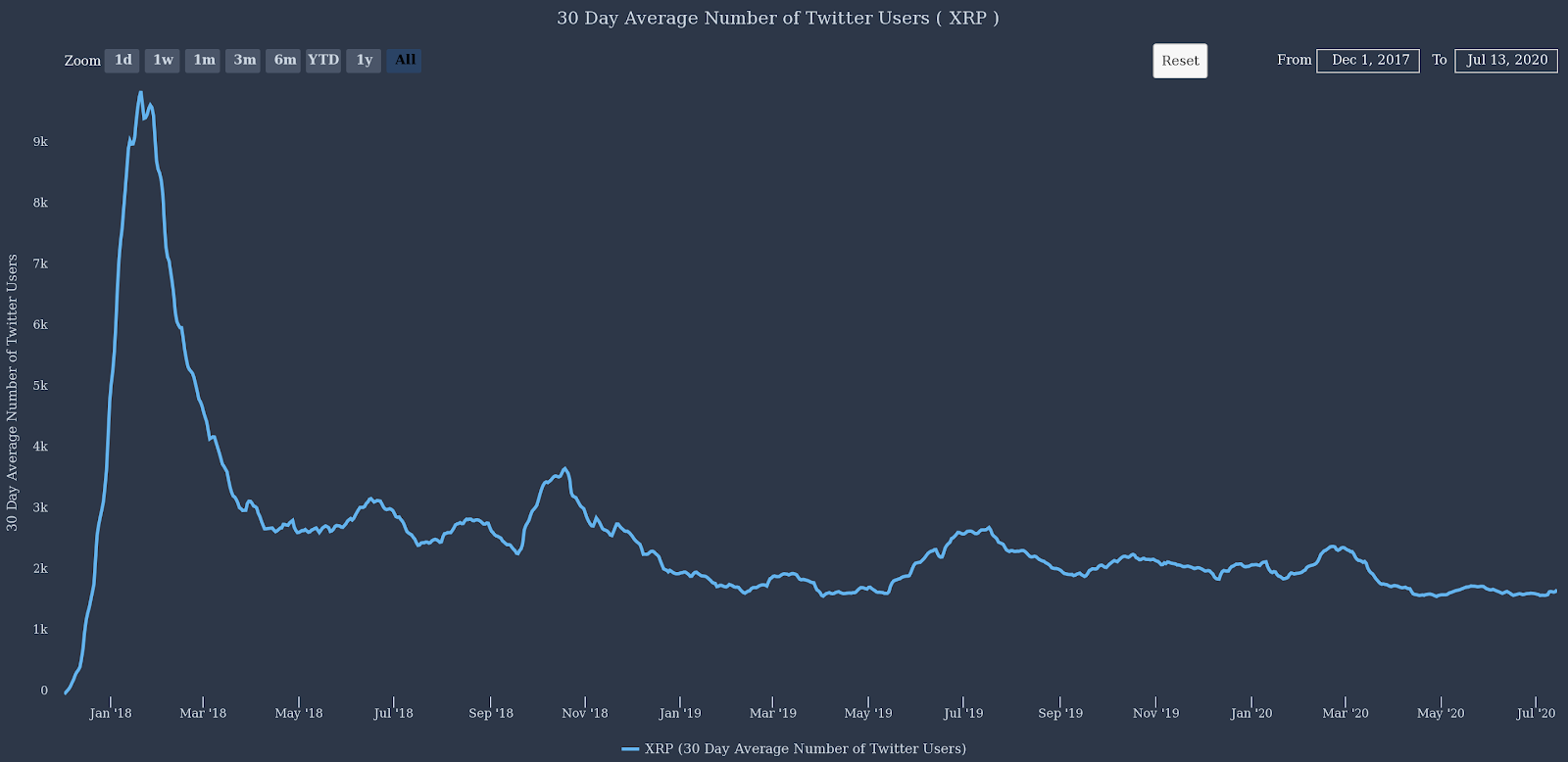

As a result, XRPL is losing the attention of retail. Even though nearly a million users follow the project’s official Twitter account, only about 0.2% of them are active.

A look at Ripple’s active Twitter users shows a similar story:

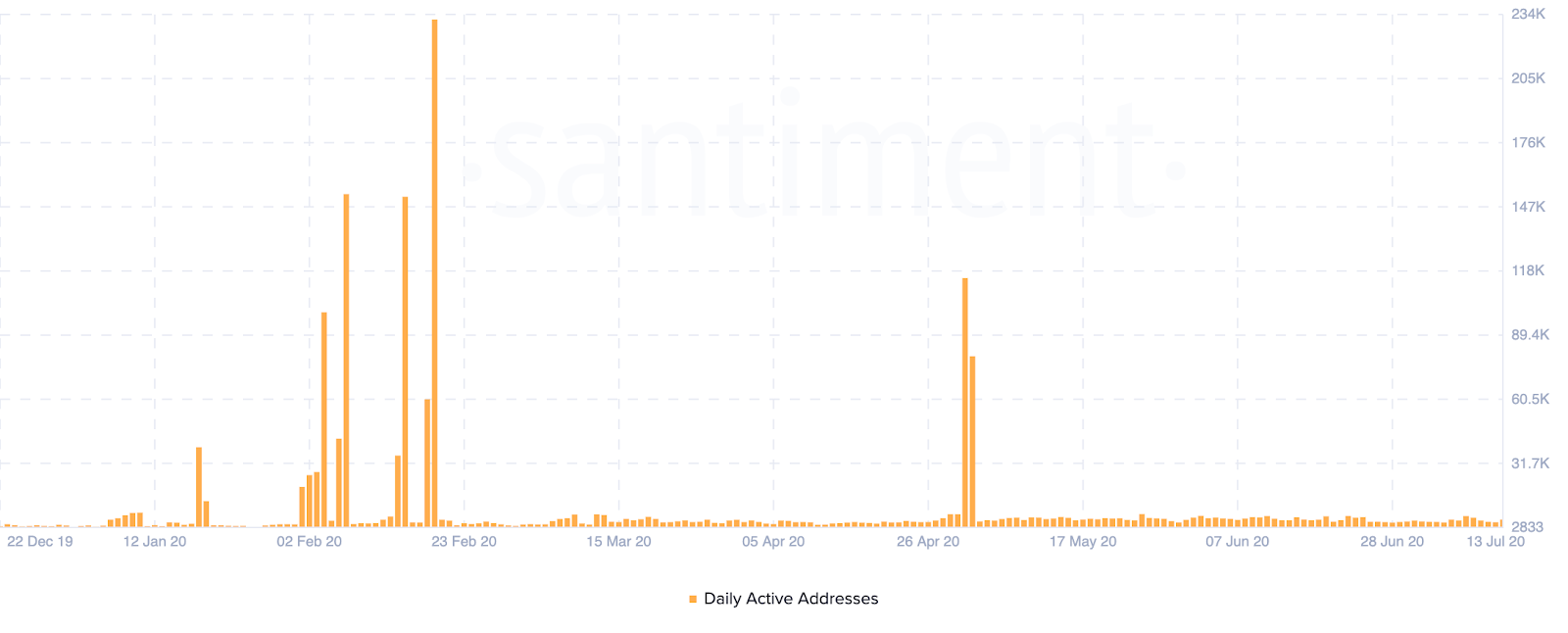

Retail usage of XRP Ledger is also flatlining. Outside of spam, genuine transaction activity is abysmal. Active addresses, an indicator of retail usage, shows that few people are using the cryptocurrency.

XRP Daily Active Addresses

That said, Flare, a project that focuses on bringing XRPL to the dApp space by implementing smart contracts, is currently in the testnet stage. If it’s successful, XRP may earn back some of the market’s attention. However, growing a developer community and a vibrant ecosystem of dApps will require more effort on Ripple’s part.

The XRP Supply Is Piling Up

Like Bitcoin, XRP has a finite supply and deflationary token economics. While Bitcoin’s deflation depends on lost tokens, XRPL has a burning mechanism that destroys coins for each transaction. If the network experiences high activity, users are incentivized to burn more XRP to push their transactions to the front of the queue.

At the current low network load of 10 transactions per second and an average transaction fee of 0.0004 XRP, the annualized burn rate is roughly 134,500 XRP (0.0001345% of the total supply). This marginal burn rate has a negligible impact on circulating supply.

The network also has a mechanism for reducing token velocity. Currently, each account on the network must hold at least 20 XRP (previously 50).

The mechanisms mentioned above would work well to influence the supply and demand ratio positively should the network become more active. But, the XRP Ledger is not actively used, adding supply pressure behind the token and causing prices to drop further.

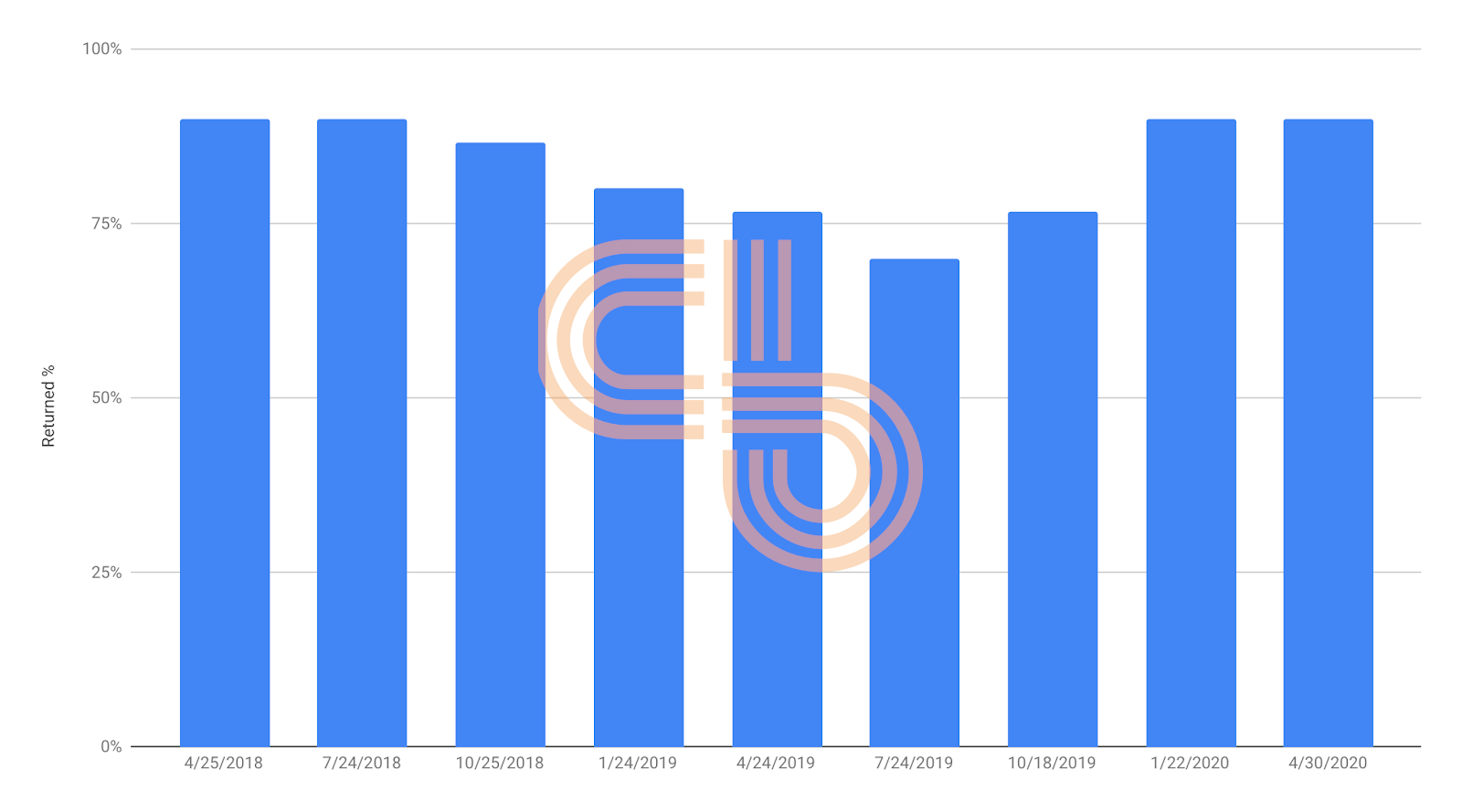

Back in 2017, the team decided to escrow 55% of the total supply of XRP. They hoped to use the gesture to build trust among institutions by making it harder to flood the market with their coins. Ripple created 55 escrow accounts containing 1 billion XRP each. These funds will unlock over the course of four and a half years.

Locking up a majority of the XRP supply had a positive impact on prices at the time of implementation. Now, the team is starting to feel the repercussions as more and more tokens get unlocked. Without substantial demand, putting all 1 billion XRP into circulation each month would destroy prices. To compensate, Ripple locks most of these tokens back up in escrow.

Percentage of Released XRP Returned to Escrow

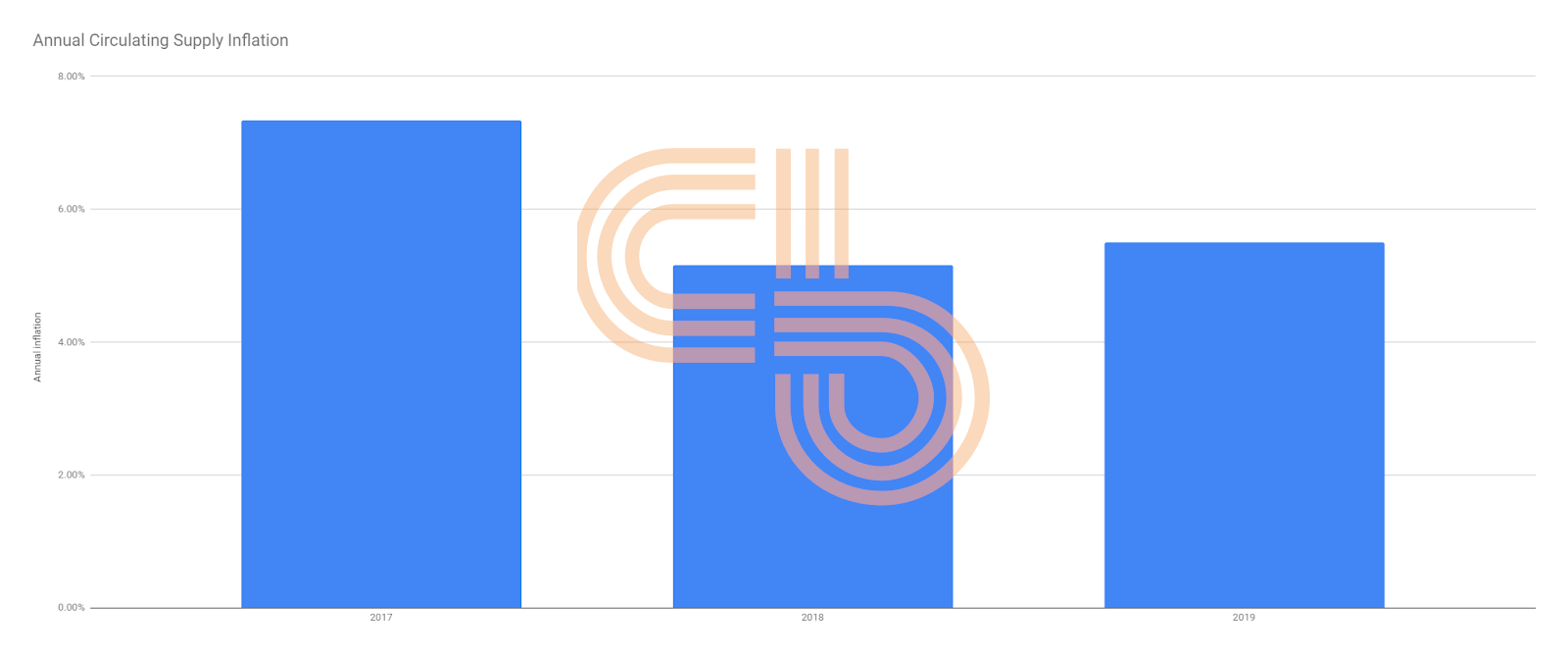

Still, Ripple has to sell some of its XRP holdings to keep the business “cash flow positive,” as the project’s CEO Brad Garlinghouse told Financial Times. Regular sales have led to a steady increase in circulating supply, amounting to about 6% inflation annually.

Annual Circulating Supply Inflation of XRP

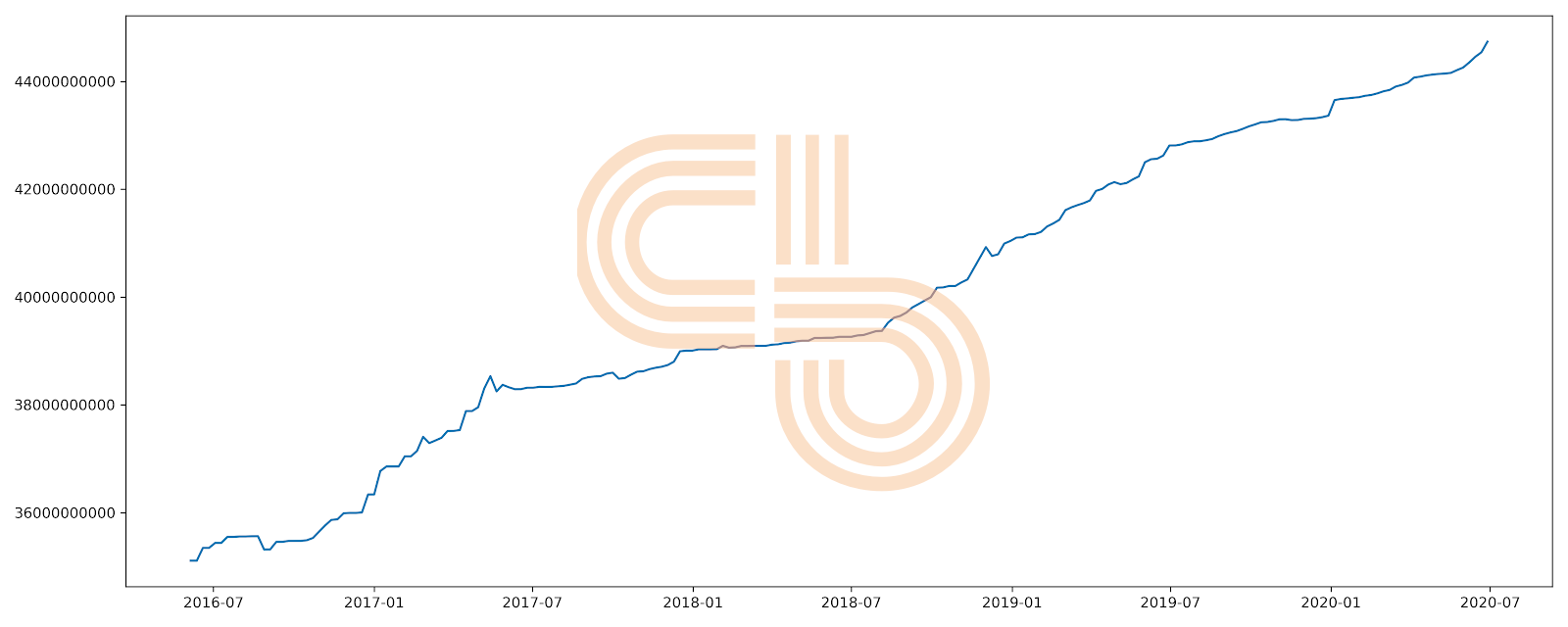

A chart of free-floating supply, which adjusts for insiders and destroyed and lost coins, again shows similar issues with inflation.

XRP Free Float Supply

XRP is still piling up in Ripple’s reserves, and it will take a long time before all these tokens are released from escrow at the current pace of the company’s sales. At the same time, inflation of the circulating supply is enough to keep XRP prices underwater given lackluster demand.

As a consequence, Ripple faces a long-lasting predicament of needing to liquidate XRP and stay afloat while trying to maintain a floor for the coin’s price.

Performance Implications

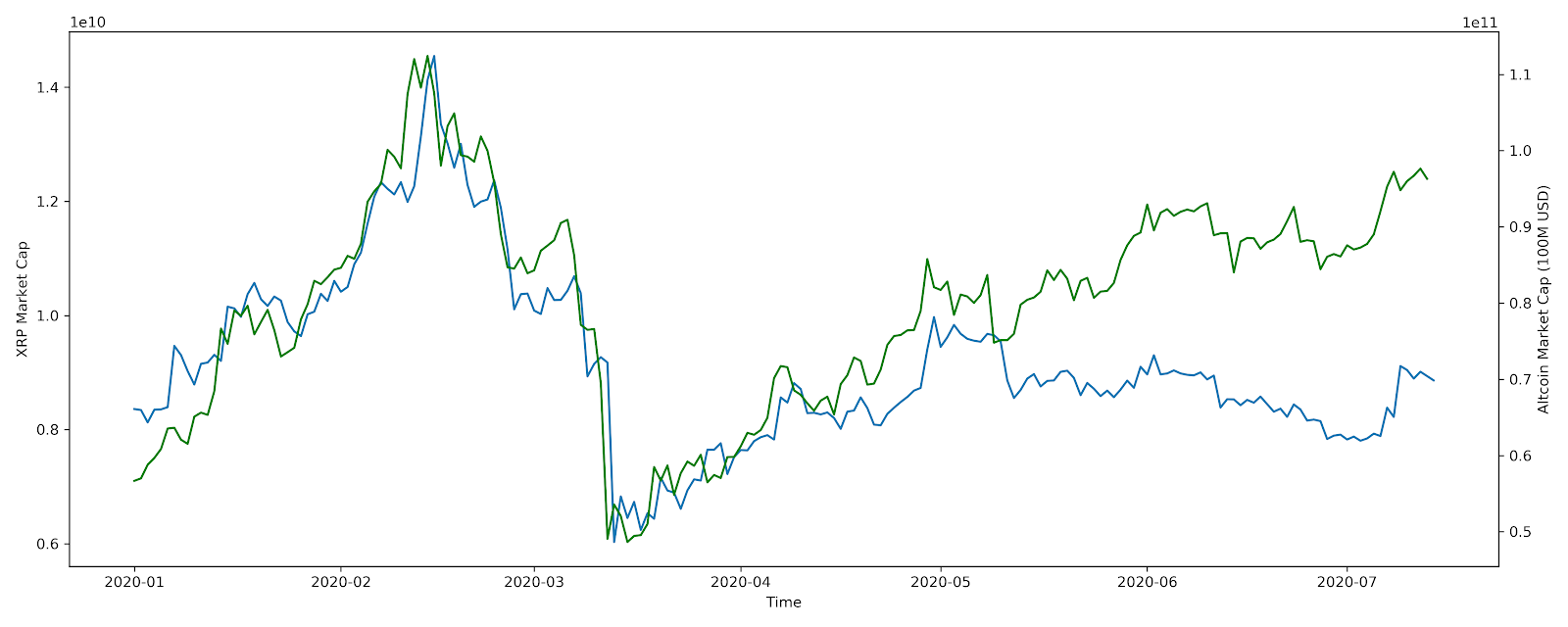

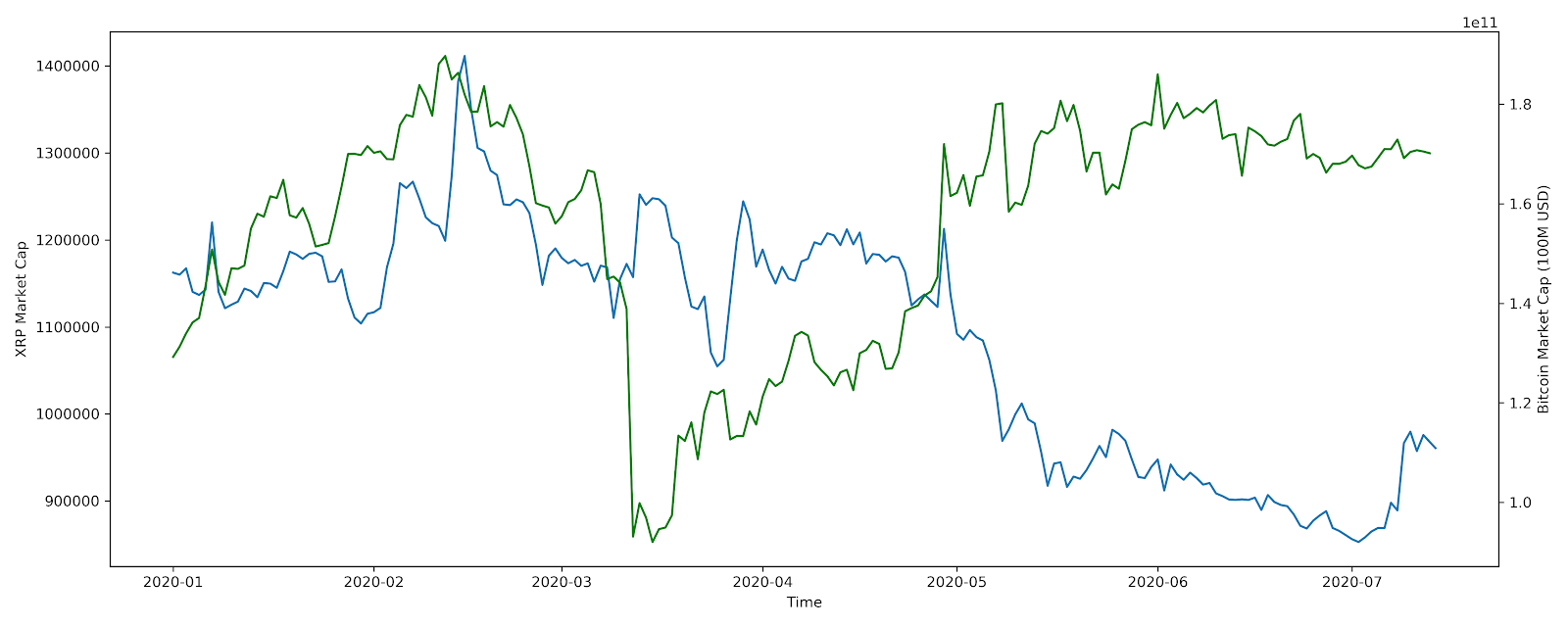

The predicament Ripple faces with its token are already manifesting itself in the coin’s price performance. While the altcoin market saw a quick rebound from devastating March lows, XRP lagged behind—both in terms of dollars and Bitcoins.

XRP Market Cap vs. Total Altcoin Market Cap

XRP Market Cap vs. Bitcoin Market Cap

Unless Ripple can facilitate organic demand for XRP, prices will continue to struggle. The possible advent of XRPL smart-contracts and its MoneyGram acquisition may drive some attention to the blockchain, but it will take Ripple a lot more than that to drive sustainable demand for its token.