Photo: Getty Images

Crypto Traders to Sue Binance for Millions After May Outage

Anyone that has lost money in the May 19 incident can join the group to pursue Binance for compensation at zero cost.

A loosely organized group of traders is pursuing Binance for compensation over losses caused by a malfunction on the exchange during one of the bloodiest days in crypto history earlier this year.

Millions Lost During Binance Outage

A group of cryptocurrency traders is suing Binance over an outage the exchange suffered in May. The Swiss litigation finance group Liti Capital has committed over $5 million to help the traders fight an international arbitration case against Binance, with New York law firm White & Case set to represent those affected.

On May 19, during a major crypto market crash that saw Bitcoin and Ethereum plummet over 30% in value, multiple sources reported that Binance’s futures and leveraged tokens products stopped working as intended. Many Binance customers suffered liquidations and lost significant sums of money as a result of the incident.

Fawaz Ahmed, an experienced Canadian crypto trader who shared his tragic story with Crypto Briefing, says he lost approximately $9 million during the incident. “I clicked the “close position” and “stop loss” buttons over 70 times within an hour. They did not work. They wouldn’t click. Nothing would happen when I tried clicking those buttons,” Fawaz recounted.

If Binance’s platform had been working like it’s supposed to, Fawaz says he would’ve walked away with 3,300 Ethereum, worth around $8.5 million at the time. Instead, he lost everything and walked away traumatized. “I have changed since May 19,” he says. “I don’t think I will be the same again. It was the worst experience of my life.”

Another trader who spoke with Crypto Briefing under conditions of anonymity lost $80,000 trading Binance Leveraged Tokens (BLVT) using algorithmic trading bots. According to him, Binance’s API malfunctioned, causing his trading bots to fail, meaning they did not sell when the market crashed.

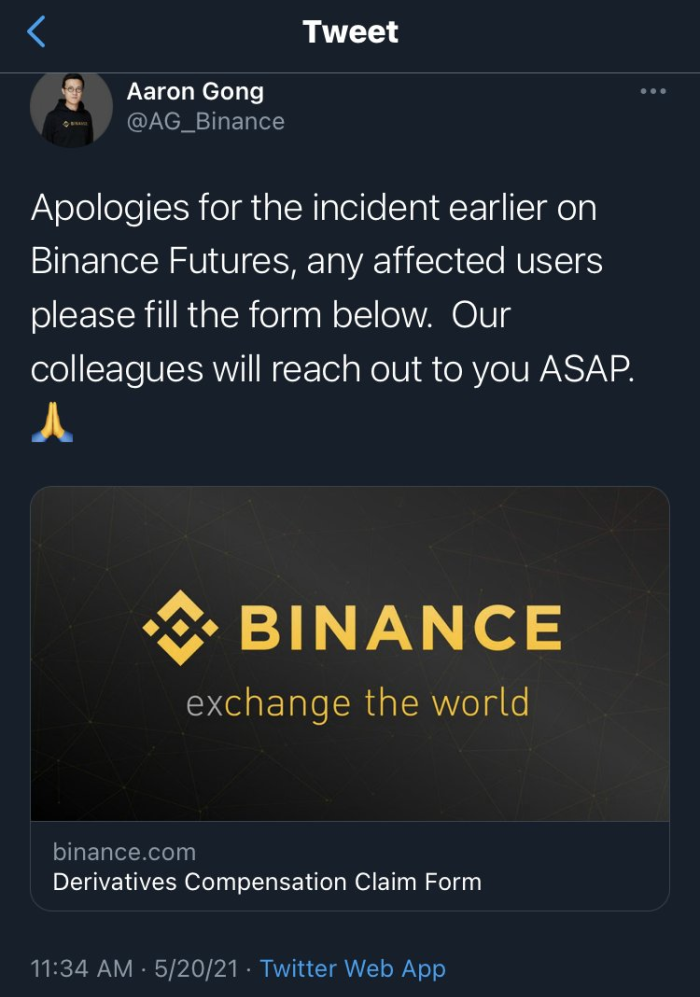

When he reached out to Binance, the exchange initially denied all liability. A customer support representative told him that it was “perfectly normal for the tokens to drop as they did.” However, on May 20, Binance’s VP of Derivatives Aaron Gong sent out a tweet apologizing for an “incident” on its Binance Futures market, promising that staff would reach out to those affected. The tweet was deleted the same day.

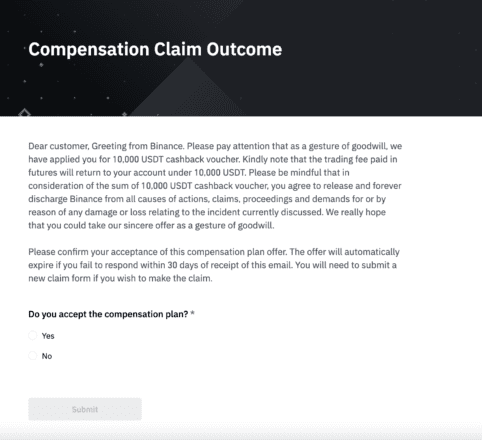

The victim pressed Binance on the issue and showed the customer support team a screenshot of Aaron Gong’s tweet. Binance offered him $18,000 worth of BLVT tokens as compensation. BLVT tokens are a leveraged Binance product representing an underlying asset; some are negatively correlated to move in the opposite direction, while others follow the asset’s price with leverage. They’re popular among day traders.

“Hours after I accepted the compensation, I got an email saying my account is flagged and that I must terminate it immediately. When I explained that if I close my account, I won’t be able to transfer the leveraged tokens out of Binance as they’re not compatible with other exchanges, they bluntly told me, ‘then you’ll have to sell,'” he says.

The API malfunction wasn’t the only issue. According to multiple video reports viewed by Crypto Briefing, Binance’s futures platform encountered problems at the height of the crash, between 12:40 and 13:10 UTC. Many traders struggled to add collateral to losing long positions, while others were completely locked out of the exchange.

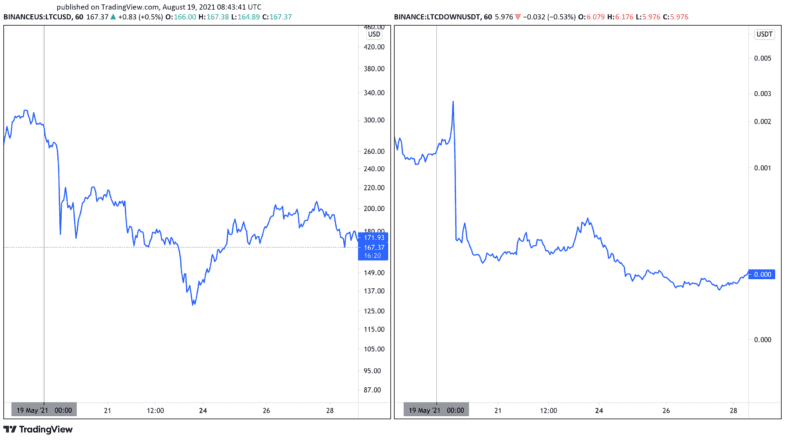

What’s more, on the day of the incident, the BLVTs failed to work as marketed. For instance, when the price of Litecoin (LTC) decreased, the LTCDOWN BLVT should have increased (there’s also an LTCUP BLVT token designed to increase when LTC does). Instead, all BLVTs crashed, resulting in many traders losing the money they had deposited.

“Binance Has Been Very Aggressive”

Aaron Gong’s deleted tweet suggests that Binance may have had plans to compensate the users affected. Instead, the victims allege that Binance took a different route. Those who agreed to any compensation plan were reportedly made to sign a contract and non-disclosure agreement.

Speaking to Crypto Briefing, Aija Lejniece, an attorney specialized in cross-border disputes and international arbitration who’s now working with Liti Capital to represent the victims, explained:

“Binance has been very aggressive. The compensations Binance offered to users came with strings attached. They said we’re not going to compensate just a tiny little bit but then made those who accepted the compensation sign a contract, releasing Binance from any other responsibility and waiving their rights to sue or ask for more money. Moreover, Binance also asked users to sign a non-disclosure agreement containing another arbitration clause that allows Binance to sue the claimants should they release information regarding this settlement plus monetary fines.”

According to Ms. Lejniece and evidence gathered by Crypto Briefing, the compensations offered range between 5% and 30% of the original losses. In Fawaz’s case, Binance offered $10,000 to compensate for his nearly $9 million loss.

“Of course I refused,” Fawaz told Crypto Briefing, but other victims accepted the offer and signed the NDA. Explaining her view on how Binance has been able to shun any responsibility for the incident, Ms. Lejniece cites two key factors: their decentralized nature, and the Terms of Use traders agree to when they use the platform. Detailing the two factors, she explains:

“One, they don’t have an official headquarters. They have a complicated corporate structure—which is normal for a lot of companies—but Binance is really not transparent. It’s not clear where they’re registered. There are many Binance entities: one is registered in Lithuania, one in Germany, the Cayman Islands, Malta, China, and so on. So it’s really hard to pin them down. Two, in terms of being sued, they’ve made their Terms of Use very restrictive for people who trade on their platform.”

“They’ll do what can be called jurisdiction hopping,” says Ms. Lajniece. In other words, Binance may register an entity in one place. If that entity disappears after two months, tracking can become very difficult. Upon registering on the exchange, users must waive their rights to any group or class actions or the ability to sue Binance as individuals in any national court. Users seeking compensation are instead required to file disputes with the Hong Kong International Arbitration Centre (HKIAC), which costs a minimum of $65,000 in fees alone—barring many from trying.

A Chance to Fight Back

David Kay of Liti Capital, which specializes in raising capital for legal cases, claims that Binance has made “pursuing justice against them unviable for most people.”

But that may not be the case for much longer, Kay insists. A loosely organized group of traders that suffered losses due to Binance’s platform failure have now formed a Steering Committee and arranged for Liti Capital to provide funding for the case and give them a fair chance to fight back.

Liti Capital has raised over $5 million to date, while the White & Case firm hired to fight the case is ranked as the best international arbitration law firm globally.

The latest group action against Binance comes at a time of increased regulatory pressure from global regulators. In the last two months alone, the U.K., Malaysia, Italy, Japan, Poland, the Cayman Islands, and Thailand have issued warnings to Binance asserting that the company is not registered and thus not allowed to operate in their jurisdictions legally. Binance is also reportedly being investigated by the U.S. Department of Justice (DoJ) and the Internal Revenue Service (IRS) concerning possible tax evasion and money laundering offenses. The exchange has since taken several steps to comply with regulators, with the firm’s CEO Changpeng Zhao recently claiming that it intends to focus on “proactive compliance.”

Binance responded to Crypto Briefing’s request for a statement explaining that it does not comment on pending legal issues. However, a representative said:

“Our policy is fair in that we compensate users who experienced actual trading losses due to our system’s issues. We do not cover hypothetical ‘what could have been’ situations such as unrealized profits.”

Liti Capital has set up a website for users affected by the Binance outage. A note reads that there is “no risk or cost” to join as Liti Capital is covering all of the funding for the case. It also says that the total loss incurred could amount to over $100 million.