Are IEOs Safer to Invest in Than ICOs?

The next era of ICOs?

After the ICO bubble popped in late 2018, projects scrambled to find new ways to raise money. After briefly courting the Security Token Offering, markets settled on a ‘new’ concept: the Initial Exchange Offering. Is this new model really an improvement over the original?

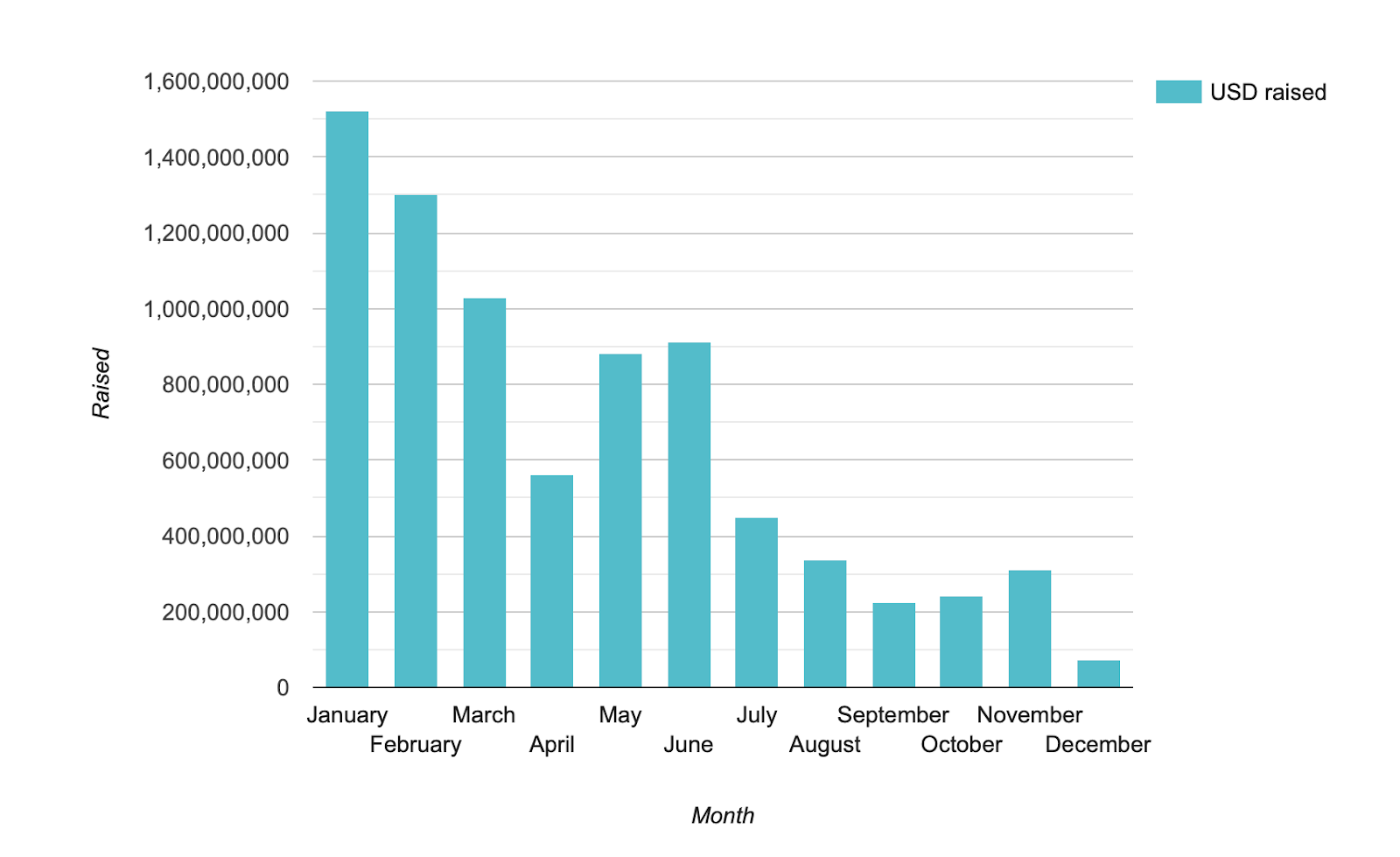

Though the ICO market quickly grew to billions of dollars in collected funds through 2017, the last months of 2018 saw funding dry up. Only $74 million was collected in December, less than what some stand-alone projects raised only a few months earlier.

The IEO: An ICO By Another Name?

Unlike ICOs, Exchange Offerings are launched in collaboration with a cryptocurrency exchange. In theory, exchanges should be screening the projects they list, only allowing ‘legitimate’ projects on their platforms.

The majority of IEO’s are ostensibly selling utility tokens that are very similar to those offered in earlier ICOs. While the regulatory landscape is complicated, the lead U.S. regulator has clearly stated that most ICO token sales are securities issuances.

This poses a sizeable degree of risk for both IEO issuers and contributors. Investing in a project only to see it entering a deathmatch against the SEC is not a particularly exciting prospect.

On a fundamental level, the formulas remain the same: give the project money, obtain tokens. However, exchanges give a valuable service to token issuers. In addition to providing a ready-made platform, they solve one of the crucial issues for any crowdfunding initiative — finding interested people.

How the IEO Popped Into Existence

One reason for the fall of the ICOs was the inability to market them. Facebook, Google, Bing, Reddit, Twitter and other digital marketing platforms all banned ICOs in the first half of 2018.

Digital ads provided a reliable and measurable medium to reach outsiders. Without them, the ICOs were left competing for a dwindling pool of existing crypto enthusiasts.

Exchanges, on the other hand, can offer a large base of hardcore crypto traders that are spurred into action through cross-promotional activities. Though it makes marketing a lot simpler, it does not mean that projects can completely disregard their own campaigns.

Projects getting their token listed was also a major issue for ICOs. By conducting an exchange offering, they are guaranteed to be available for trading on at least that platform.

For the users, the benefits seem to be clear. The due diligence conducted by exchanges should, at the very least, discourage outright fraud, though there are few guarantees of actually making a good investment. In fact, investment returns have generally been lackluster so far — at least partially because of some questionable choices made by some IEO platforms.

Some Exchanges Are More Diligent Than Others

While the additional layer of intermediation should help, the quality of the projects still falls on a wide spectrum.

Binance, which kickstarted the IEO phenomenon with the BitTorrent sale, makes a point of researching and vetting all important aspects of a project.

For example, the upcoming TROY IEO features a detailed report from Binance Research that focuses specifically on investability. It covers key value proposition, token release schedules, partnerships, teams, development activity on GitHub and many more. The exchange only conducted nine IEOs so far — a testament to its selectivity. Due to this and other factors, Binance is doing better than its competitors in terms of return on investment.

But other IEO platforms are less successful. Both OK Jumpstart and Huobi Prime tend to value tokens vastly below market rate on listing, increasing the publicity and the sell-out rate of their offerings.

That may not be enough, as OK Jumpstart tokens show. X-power Chain, the latest IEO on the platform, is still above sale price at the time of writing. However, older sales, such as Eminer, Pledgecamp, and Blockcloud all lost more than 90 percent of their value within months of their IEOs. This is not standard behavior and likely indicates deep-rooted issues in these projects.

Unlike with Binance, these platforms only offer minimal information concerning token allocation. The discovery of the project is left to the individual user.

Most of the better known exchanges offering IEO platforms had, at most, a dozen token sales, suggesting that there is at least some degree of filtering. Tokinex only had three, but thanks to the LEO sale, Bitfinex is responsible for about two thirds of approximately $1.5 billion raised in IEOs.

But then there are platforms like LATOKEN. The exchange features dozens of previous and upcoming IEOs.

Some of the past and present token sales include: Stellar Gold, whose whitepaper — in broken English — features standard blockchain gibberish and invokes Satoshi’s vision (not the technology); ASTRcoin, a project that is supposed to secure claims for asteroid mining; Rasputin Party Mansion; and Gleec, a Bitcoin fork project using a badly synthesized voice for its introduction video.

The platform does feature its own rating system, but it is one where projects such as Gleec and ASTRcoin received the maximum score. Though some of them may be legitimate, Latoken’s IEOs bear an uncanny resemblance to the ICOs of old. Compared to the other platforms, Latoken held more than 140 IEOs since its launch in 2017, a source of pride for the team.

The Latoken team provided commentary to Crypto Briefing on some aspects of its exchange. They noted that the rating system is not an indication of the investment quality of the project, but rather the result of basic background checks:

“Following our mission to connect contributors and entrepreneurs, we made the Verification score on LATOKEN IEO Launchpad so that investors analyzing IEOs can save time on fact-checking on basic information including the token issuer, the team background, the previous fundraising rounds, notable advisors and partnerships.”

Latoken CEO Valentin Preobrazhenskiy also explained that the exchange doesn’t see itself as an investment advisor, thus providing no additional filtering beyond basic legitimacy guarantees. The platform does not charge a fee for IEO listing, instead taking a percentage of the collected funds. It does however charge for listing the token on the actual trading platform, which is a mandatory option.

Contributing to token sales was — and still remains — a risky proposition. Though some exchanges embraced the role of gatekeepers for their contributors, others only provide limited guarantees. The line between an ICO and an IEO can often be quite blurred.

This article was updated with commentary from Latoken.